The end of the year is fast approaching (although some would say 2020 can’t finish fast enough!)

But, there’s still time to make moves to improve your financial plan and tax situation before the calendar turns.

We’ve got you covered with our 2020 year-end planning guide.

1. Maximize Your Retirement

The IRS recently released their Contributions and Benefit Limits for 2021. Unfortunately, there will not be an increase in either 401(k) salary deferrals or the catch-up contribution for those age 50 or older.

Planning Tip: Don’t forget to maximize your 401(k) contribution for the year if you have the means. And if are 50 years or older (or will turn 50 years old anytime during 2020), you are also eligible for the catch-up contribution! Make sure you have contributed both the $19,500 deferral and the $6,500 catch-up maximum for this year. Then, in January, make sure you elect to defer the new higher amount in 2021.

You can download this chart here: 2021 Table of Contribution Limits.pdf

2. Maximize Your Health Savings Account (HSA)

HSAs can be a powerful savings tool for high income families. In fact, they are the only investment vehicle that deliver triple-tax benefits. Contributions are tax-deductible, earnings are tax-deferred, and withdrawals are tax-free when used for qualified medical expenses.

You can read more about HSAs here.

If you are covered under a high-deductible-health-plan you have until the end of the year to maximize your contribution.

For 2020, a high-deductible-health-plan is defined as one which requires minimum annual out-of-pocket deductibles of $1,400 for an individual and $2,800 for families. Yearly out-of-pocket expenses (including deductibles, copayments, and coinsurance) cannot be more than $6,900 for an individual or $13,800 for a family. You also must not be enrolled in Medicare, covered by another health plan that is not a high-deductible-plan, or claimed as a dependent on someone else’s tax return.

Planning Tip: You have until April 15th to maximize contributions and have them count for 2020.

3. Maximize your Charitable Contributions

In 2020, the standard deduction has increased to $12,400 for single filers or $24,800 for married, filing jointly. To take advantage of itemized deductions such as mortgage interest, state and local taxes (SALT), and charitable contributions, the total of these deductions must exceed the standard deduction.

If you’ve had an unusually high income this year (thanks to a bonus, sale of a business, etc), you can use charitable bunching by making a larger than usual tax-deductible contribution to a Donor Advised Fund (DAF). Bunching allows you to advance your next few years of charitable gifts into the current tax year. The aim is for this deduction to exceed the standard deduction so you can minimize your taxes today. In future years, you can direct your DAF to make gifts to charities on your behalf - with the timing and dollar amount of your choosing.

You can read more about DAFs and making the most of your charitable contributions here.

Planning Tip: Cash is not always the most efficient asset to give to charity. Consider donating highly appreciated securities to a Donor Advised Fund to minimize taxes and maximize your charitable contribution.

4. SECURE ACT and CARES ACT

The SECURE ACT was signed into law last December and provides two enhancements for retirees and pre-retirees.

- Required Minimum Distributions (RMDs) from IRAs/401(k)s were pushed back to age 72. This allows an extra 1 ½ years of additional compound growth and tax deferral over the old rules.

However, under the CARES ACT, RMDs have been waived for 2020 due to the pandemic. So, if you are 72 or older and have been waiting until the end of the year to take your RMD, your procrastination paid off!

- Contributions to Traditional IRAs can be made at any age. Under the old rules, contributions were disallowed after reaching 70 ½. If you have earned income and a desire to pad your Traditional IRA, there’s still time to make a contribution.

Planning Tip: Contributions to IRAs can be made up to April 15th to be counted for 2020.

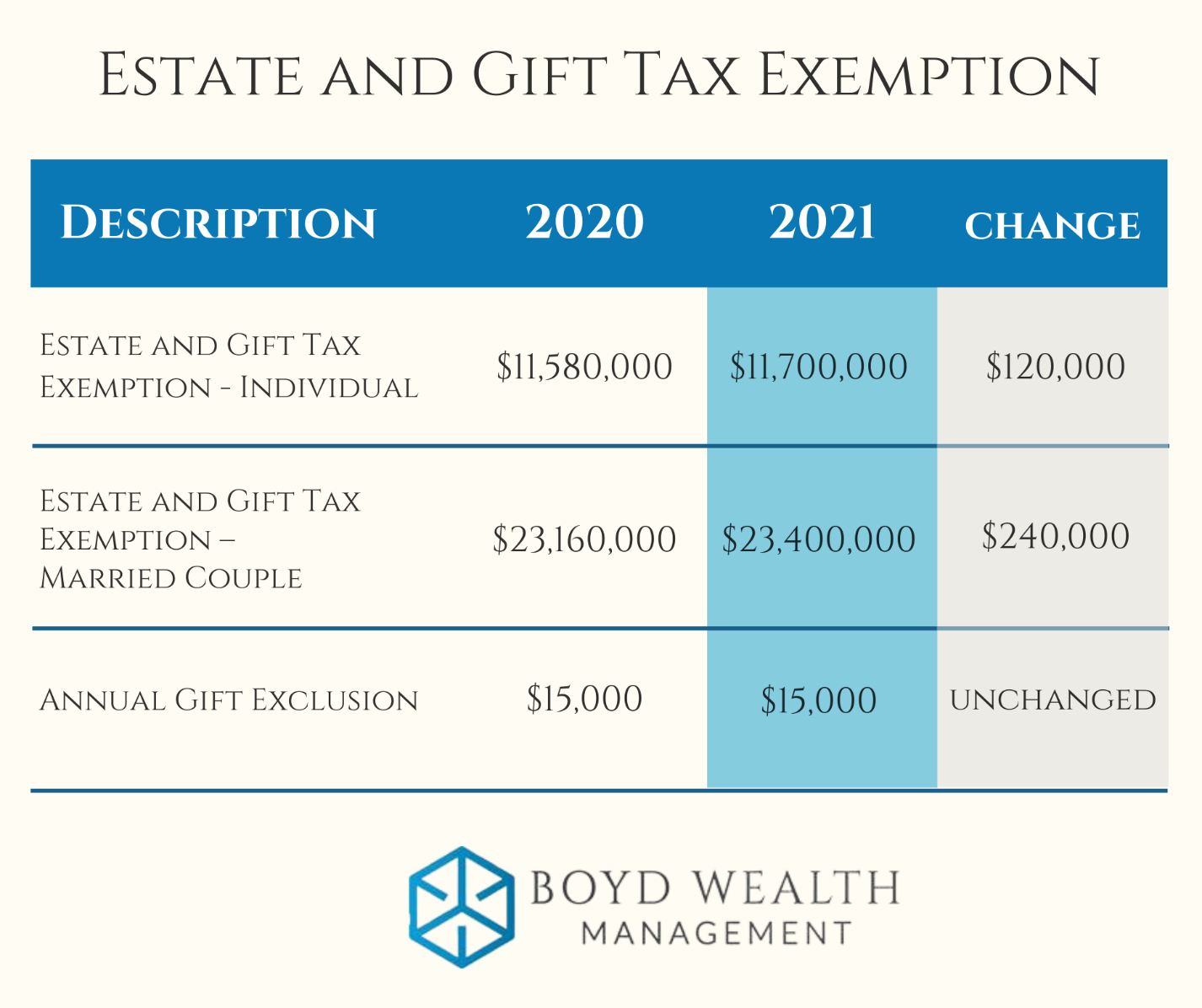

5. Gifting to Loved Ones

With (most) of the election in the rear-view mirror, the outcome suggests we likely won’t see major tax changes in 2021. However, the estate tax could be “low hanging fruit” for alterations because it currently affects less than an estimated .10% of the population.

President-elect Biden has proposed restoring the estate and gift exemption amounts to their 2009 level: $3,500,000 per person for estate tax, $1,000,000 for gift tax, and a top rate of 45% (up from the current 40% rate.).

It’s too soon to tell whether there’s support for any of these changes, but if you were interested in transferring wealth to children or grandchildren this may be your year to do it.

It’s important to note that anyone can give up to $15,000 of tax-free gifts per person, per year. Annual gifts do not rollover, so it’s use it or lose it.

Planning Tip: Because the annual gifting limit is $15,000 per person, a husband and wife with two married children and four grandchildren could gift a total of $240,000. (That’s $15,000 to each of the 8 family members, from both husband and wife, or $30,000 x 8!)

6. Make a Qualified Charitable Distribution (QCD)

One of the most exciting aspects of the Pension Protection Act of 2006 was the Qualified Charitable Contribution, or QCD. A QCD allows you to make a charitable donation up to a maximum of $100,000 per person/per year to a charity, with the amount donated directly offsetting the Required Minimum Distribution.

For high-net-worth individuals in the RMD stage, we find they typically receive more in required distributions than they want or need. By donating to your favorite charity directly from an Individual Retirement Account, your required distribution and taxes are reduced under the QCD method. This is especially important for those unable to itemize their deductions, as now their charitable donations can be taken in full. If you are currently taking RMDs and making charitable donations, QCD’s can be a fantastic strategy.

Planning Tip: Review your ongoing and upcoming charitable gifts and create a plan to do that in the most efficient way possible.

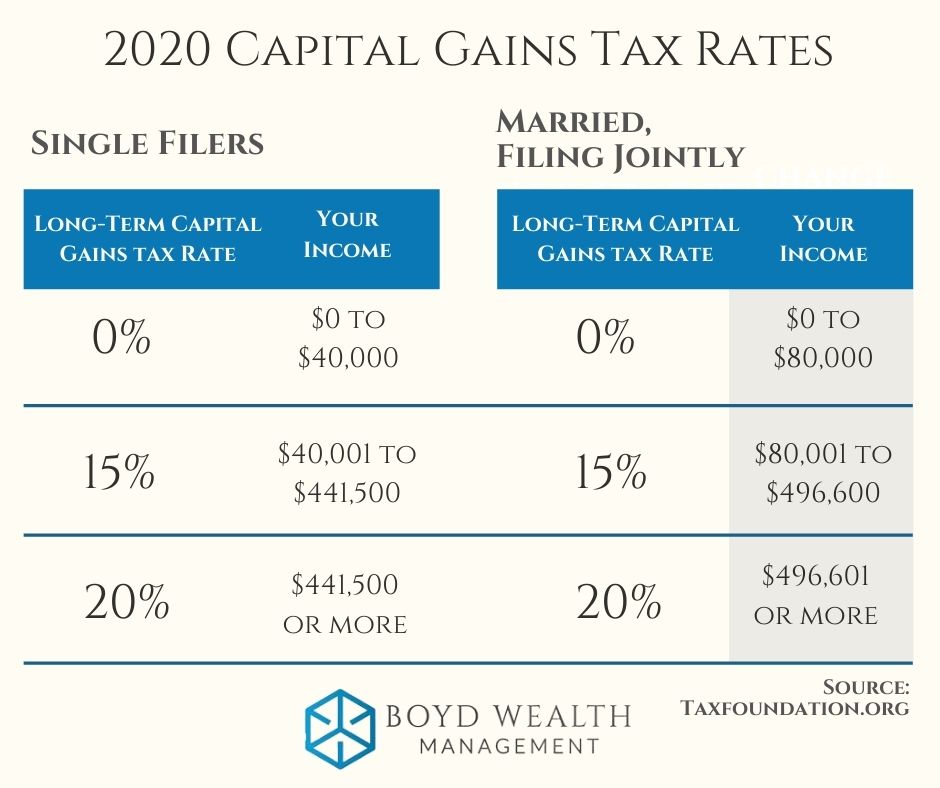

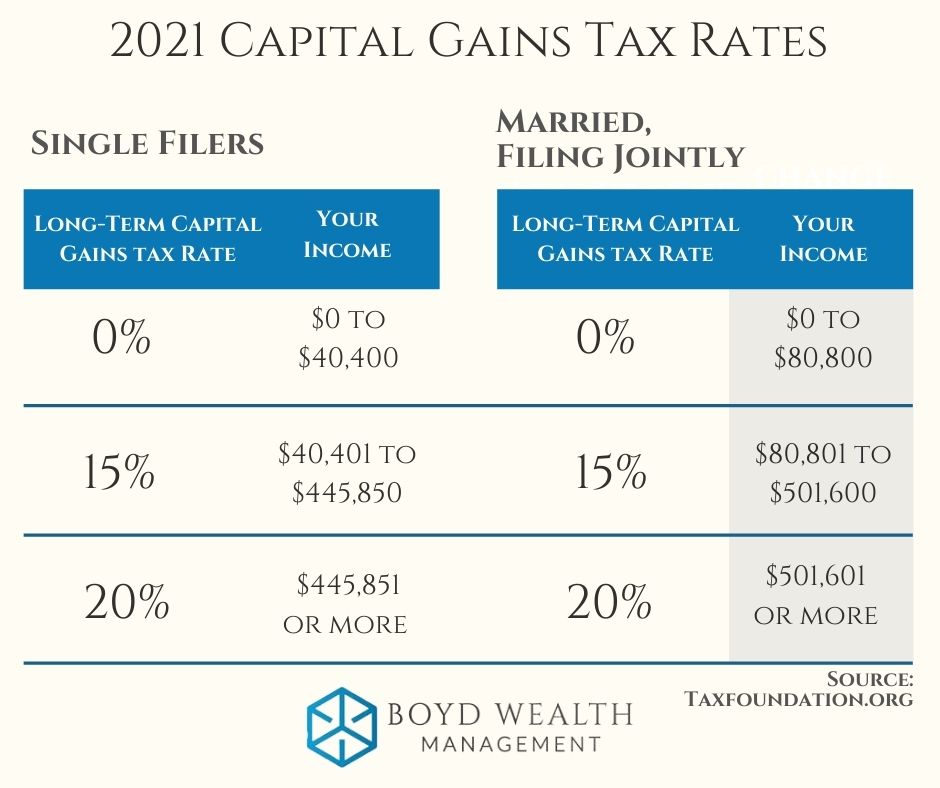

7. Tax Gain Harvesting

This has been a challenging year for investors, particularly between the months of February and August. However, through October 31st, most diversified portfolios are showing slightly positive year-to-date returns.

We’ll talk more in the future about the positive impact of tax loss harvesting during a sharp market downturn, such as we had in 2020. But tax gain harvesting is something to consider before year end. With tax gain harvesting, you’re selling appreciated securities and recognizing taxes in the current calendar year because you expect to be in a higher rate next year.

For retirees who diligently maintain a cash bucket/emergency fund, replenishing that cash back to target could be a good idea before year end. While raising cash may result in realizing capital gains, with equities close to all-time highs (as of this writing), it makes sense to peel off gains. Plus, for those with banked tax losses from the downturn, some or all of these gains may be offset.

Another way to manage gains would be to sell low basis stocks in your portfolio which either may not fit in your plan anymore or aren’t expected to do well in the future. If you are having a low(er) income year in 2020, but expect a big tax year in 2021 (perhaps from business sale, bonus, or stock compensation), now may be the time to recognize gains on that position. You can then reallocate the proceeds to your target diversified portfolio.

Gains from positions held less than one year are short term capital gains and are taxed at ordinary income tax rates.

Planning Tip: We all lack perfect information when making financial planning decisions. In this case, it’s impossible to know the direction of future tax rates. Gather all relevant projected income and tax information for the year and make the best decision you can with the information you have.

8. Roth Conversion

On the same note, if you are experiencing a low-income year, consider converting all or a portion of a Traditional IRA to a Roth IRA. Doing so means you’ll recognize income today on the amount converted, but withdrawals in the future will be tax-free.

Say you anticipate a near zero earned income. The first $19,750 (for married filers) comes with a 10% federal tax rate. It’s only 12% up to $80,250. You may consider converting up to the first two brackets if your expected income in the future (earned income, Required Minimum Distributions, Pension, etc.) will be higher.

If you’re carrying a loss on your tax return, you could convert Traditional IRAs to Roth essentially tax-free as you eat into the loss.

It’s worth a discussion with your CPA and financial advisor.

Planning Tip: Converting from Traditional to Roth is not an all or nothing proposition. You can make partial conversions and spread them out over several years.

9. Update Your Beneficiary Designations

The end of the year is a great time to make sure your beneficiaries are current. Log into your 401(k) plan, speak with your HR administrator, call your financial advisor, email your life insurance agent. Request a review of your designations to verify that they match your current wishes.

Life transitions, such as divorce or the death of a spouse, are incredibly difficult. It’s understandable that during these challenging times beneficiary designations are overlooked and left unchanged. This is your reminder to review them.

Planning Tip: Whatever you have listed on a beneficiary form usually overrides what is written in your will or trust. A beneficiary form provides its own direction for the asset it covers so make sure it accurately reflects your wishes.

We hope you have a wonderful Thanksgiving and great holiday season. Don’t forget that now is an ideal time to check in and make sure your financial house is in order. Please reach out to us and/or your tax advisor to talk through any of these planning opportunities.

Wishing you a great 2021!

Happy Planning,

Brian