Investors have been on a wild ride the last 14 months. The U.S. stock market began 2020 on a high note only to collapse 34%, leading to a March 23rd COVID-induced low. From there, the market would reverse course in a big way, rising 69% through the end of the calendar year1.

But now, as we approach the halfway point of 2021, we find ourselves in the midst of the largest monetary experiment in history, with low interest rates coupled with unprecedented government spending. I’m often asked my opinion on how this will ultimately play out.

The frank answer is I don’t know. No one knows - there’s no historic precedent for this.

What I do know is that regardless of economic, market, and fiscal conditions, there are generally only four financial elements that the average person can control. In order to build and maintain a “rich” life, it’s best to focus on these things.

There is something in this post for everyone, so feel free to share this with the teens and young adults in your life.

So, what are the four elements you can control for a rich life?

1. How Much You Earn

For most people, the single largest determinant of financial success is the amount of money they earn over their lifetime.

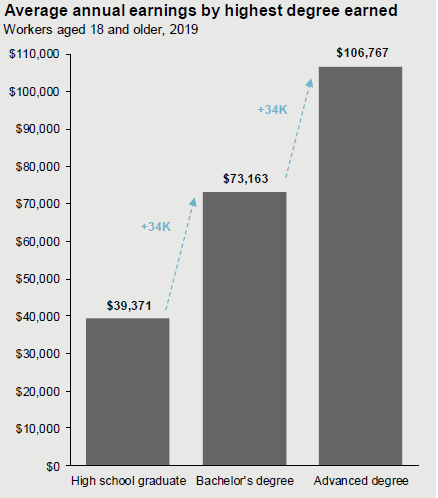

Evidence suggests that there’s a strong correlation between your wealth and the level of education attained.

According to the Social Security Administration:

“Men with bachelor's degrees earn approximately $900,000 more in median lifetime earnings than high school graduates. Women with bachelor's degrees earn $630,000 more. Men with graduate degrees earn $1.5 million more in median lifetime earnings than high school graduates. Women with graduate degrees earn $1.1 million more.”

Annually, those with a bachelor’s degree earn roughly $34,000 more per year than those with a high school diploma. Similarly, those with an advanced degree earn roughly $34,000 more per year than those with a bachelors.

Source: J.P. Morgan Asset Management; Census Bureau. Unemployment rates shown are for civilians aged 25 and older. Earnings by educational attainment comes from the Current Population Survey and is published under historical income tables by person by the Census Bureau. Guide to the Markets –U.S. Data are as of March 31, 2021

Job security (and therefore lifetime income) is also enhanced according to the level of education attained. According to the US Bureau of Labor Statistics, in 2020, the rate of unemployment for those with a high school diploma was 70% higher than those with a bachelor’s degree.

In general, the higher your level of education, the higher your income and the more stable your earning power. Obviously, the higher your income level and stability of your earnings, the more you can save or invest to build wealth.

2. How Much You Spend

My least favorite term in finance is the word “budget”. The word immediately conjures up thoughts of thrift, sacrifice, and going without. But true financial success rarely equates to living a life of frugality. On the contrary, to be wealthy is to live a balanced life - enjoying the fruits of your labor today while being conscientious of the future.

Putting the word “budget” aside, money comes in and money goes out for all of us on a monthly basis, so our spending should be measured. What gets measured gets done, as they say! Tracking your spending allows you to make simple adjustments if spending starts trending above income.

Tracking your spending is easier than ever, and it’s a great way to exert control over your financials. There are several software programs that make this near-effortless, and our Boyd Wealth Planning Portal also does this effectively. Just link your spending accounts, such as credit cards and checking, in the portal and your transactions feed through automatically.

Most purchases will auto-categorize for you based on the millions of transactions the software sees over time. Then, once per week or so, you can log into the portal and make sure things have been categorized correctly. At the end of the month, you’re left with a clear picture of how much came in and how much went out.

This process is liberating!

3. How Much You Save

As Albert Einstein once said, “Compound interest is the eighth wonder of the world. He who understands it, earns it; he who doesn't, pays it.”

Tracking your income and spending provides a clear financial picture, which allows you to save and invest diligently.

For those just starting out, time is on your side. Perhaps you’ve seen a version of this chart I created, but the impact of starting to save when you’re young is staggering:

Mary begins depositing $6,000 per year into her Roth IRA starting at age 25. She does this every year until age 60 when she retires. Assuming an average annual return of 8% per year, she has a balance at retirement of $1,033,900.

Dan gets started 10 years later at age 35 and saves aggressively by deferring $14,000 per year into his company Roth 401k. Assuming the same 8% per year average rate of return, he has an account balance of $1,023,483 at age 60.

They both end up with virtually the same balance, but Dan had to save an additional $140,000.

Save early and save often – and stay invested as long as possible!

4. How You Invest

You can’t control the ultimate performance of your portfolio, but you can control your investment process. Here are some ways to do that:

Diversify

We’ve all heard the saying that you shouldn’t put all your eggs in one basket. This definitely applies to investing, too.

Different assets perform at different times through various market and economic cycles. It’s impossible to consistently predict which individual stock, asset class, sector, or even country will be the top performer. So, spread your dollars over multiple investments such as stocks, bonds, real estate, and cash.

Align your risk tolerance, time horizon, and goals

You can also control how much risk you’re willing to take in order to reach your goals.

There is no one size fits all approach to this. Everyone has their own threshold for pain when it comes to normal (and sometimes sharp) downturns in the stock market. The portfolio that is right for you allows you to stay the course over the length of your investing horizon.

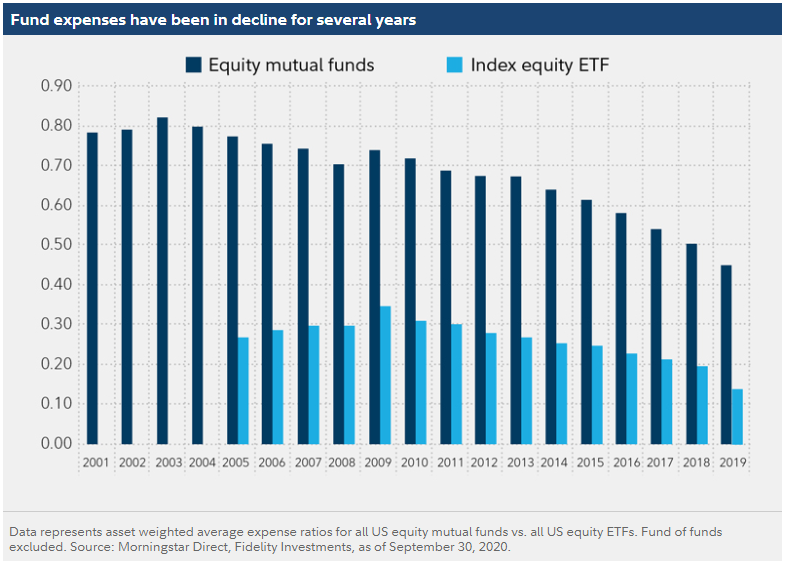

Keep your investment expenses and taxes low

When it comes to the cost of investing, the wind is currently at the backs of investors, as investment expenses have declined for a number of years now.

According to Fidelity Investments, “Several factors have contributed to the trend, including expense ratios varying inversely with fund assets, a shift toward no-load share classes for long-term mutual funds, economies of scale, investor preferences, and competition from ETFs (Exchange Traded Funds).”

There is seldom good reason to pay for expensive and/or complex exposure to an asset class.

Taxes can also have an enormous impact on long-term returns. Frequent trading and attempts at market timing can result in realizing both short-term capital gains (for assets held less than one year) and long-term capital gains. For California residents, a top combined Federal and State short term capital gains tax rate of 54.1% can decimate returns.

Control your behavior

Investor behavior is so important, we devoted an entire piece on the subject.

After implementing a diversified asset allocation that matches your risk tolerance and time horizon, you must resist the temptation to change strategy based solely on short-term market movements or emotion.

We’ve shared the chart below previously, but it bears repeating.

A hypothetical investment in the U.S. stock market for the 20-year period between 2001 and 2020 would have produced an average annual return of 7.4%.

But if you missed just the 10 best days (because you flip flopped between stocks and cash), it would reduce that return to only 3.3% per year. Missing the 30 best days in that 20-year period turns the return negative.

Bottom Line

Remember these four element the next time your Uncle Larry, your golf buddies, or the pundits on TV cause you to question your whole financial strategy.

You can live a rich life just by narrowing your focus to these four things you can control.

Please reach out if we can assist you, a friend, or a family member with any of these items.

Happy Planning,

Brian

Sources/Further Reading:

1. S&P 500 (SPY), Total returns, Data from Koyfin

https://www.ssa.gov/policy/docs/research-summaries/education-earnings.html

https://www.newyorkfed.org/research/college-labor-market/college-labor-market_wages.html