Anthony Kim was only 22 years old in 2007 when he made his presence known on the PGA tour. In 2008, he won two tournaments and propelled the US team to a Ryder Cup victory with his head-to-head win over Sergio Garcia. That year, he also earned $4.7 million, finishing sixth on golf’s overall money list.

In 2009, Kim set the record for most birdies in a round at the Masters tournament. The very next year, he took third place, right behind the incomparable Phil Mickelson who ultimately hoisted the trophy.

However, even as his promising career flourished, Kim would begin to suffer nagging injuries. First, it was a thumb injury which required surgery. Then, it was severe tendinitis in his wrist. In 2012 his Achilles heel tendon exploded while on a beach run in San Diego.

While none of these injuries alone would be enough to end a budding PGA tour career, collectively they ended Kim’s.

Winning on the PGA tour is incredibly difficult. There are no guarantees, no contracts. The travel is constant, and the financial responsibility is great for a golfer whose team generally includes a caddy, swing instructor, nutritionist, and performance coach.

It is a well-circulated rumor that early in Kim’s career, he took out an insurance policy which would protect him in the event of a career ending injury. That policy would pay him a reported $20 million if he walked away from the game forever.

Faced with the prospect of additional injuries, more travel, and loads of uncertainty, Kim cashed in on the policy and retired from the spotlight and professional golf.

Anthony Kim’s story highlights a very specific case for insurance, but risk management plays an incredibly important role in any sound financial plan. I understand that talking about insurance is less than exciting, but knowing your risks are covered appropriately can provide a sense of relief.

So, today I’ll offer a few tips to ensure you’re getting the most out of your insurance policies.

Homeowners and Auto

Home values have skyrocketed since the start of 2020 and so too have construction costs. The prices of lumber, copper, and concrete are still at or near all-time highs. These elevated material prices, along with increased labor costs, may leave you underinsured on your homeowner’s insurance policy.

Therefore, it’s a great time to schedule a review with your property and casualty insurance agent. Here are some things to consider as you review both your home and auto coverage:

• In the event of a loss, is your current coverage adequate to rebuild your home and replace its contents?

Many policies have an extended replacement cost rider which can provide an additional 25-50% of coverage above your policy’s base amount. But many do not.

This policy endorsement acts as a buffer for economic climates like this when the cost of labor and materials is high. Even if you have this coverage, it’s important to check your limits. There are usually rules that say your base coverage must be at least 80% of true replacement cost to qualify.

• Does it make sense to increase your deductibles for property coverage on your homeowner’s policy?

For high-net-worth families with sufficient liquid assets, opting for higher deductibles can lower your annual insurance premiums. This can be a good form of risk management for those adverse to filing claims.

According to Kayti Jones of Beach and O’Neill Insurance Associates in Citrus Heights, California, “Get creative and balance your risk. If you’re not going to turn in a smaller claim for fear of a rate increase or cancellation, then why not have a higher deductible?”

• What about deductibles for auto insurance?

The comprehensive portion of an auto policy covers things like theft, a cracked windshield, or even a tree falling on your car. The premiums for this part of your policy are small, and claims don’t count against you when determining your premium. However, Jones warns, “The collision portion of your auto policy carries the biggest premium and any claims stay with you for 3 years.”

One strategy for high-net-worth families is to reduce the deductible for comprehensive (to perhaps $100) and increase the deductible for collision (to perhaps $1,000). If you’d be reluctant to file a collision claim to avoid higher future premiums or even cancellation, then why pay more for a lower deductible?

• Do you have service line coverage?

Covered losses from a burst pipe or leaking sewer line are limited to repairing damage to the home. It is now common for this coverage to be added as an endorsement to your policy which also covers the cost to excavate and fix pipes, including sewer lines damaged by roots. “You can add $20,000 to $25,000 of coverage for very little premium,” says Jones.

• Do you have roadside assistance?

These policies are much more comprehensive than just providing you with a tow. If stranded, you can also have your battery jumped or replaced. These roadside heroes can even bring you gas if you accidentally run out! Many drivers believe these policies come standard with a new car or are included in all auto policies, but they are not, so be sure to ask about it.

• Are you bundling your insurance policies with one company?

Having your home, auto, and umbrella policies with a single company usually (although not always) result in an overall premium savings. It’s worth reviewing.

• Have you recently taken inventory of your possessions and home finishes?

If not, take out your iPhone, hit record on your video, and start walking around your home. Open cupboards, drawers, and closets. Don’t forget the garage! Store this video in the cloud and set a reminder to do this again in one year. This will make the potential claims process easier and ensure you are indemnified properly.

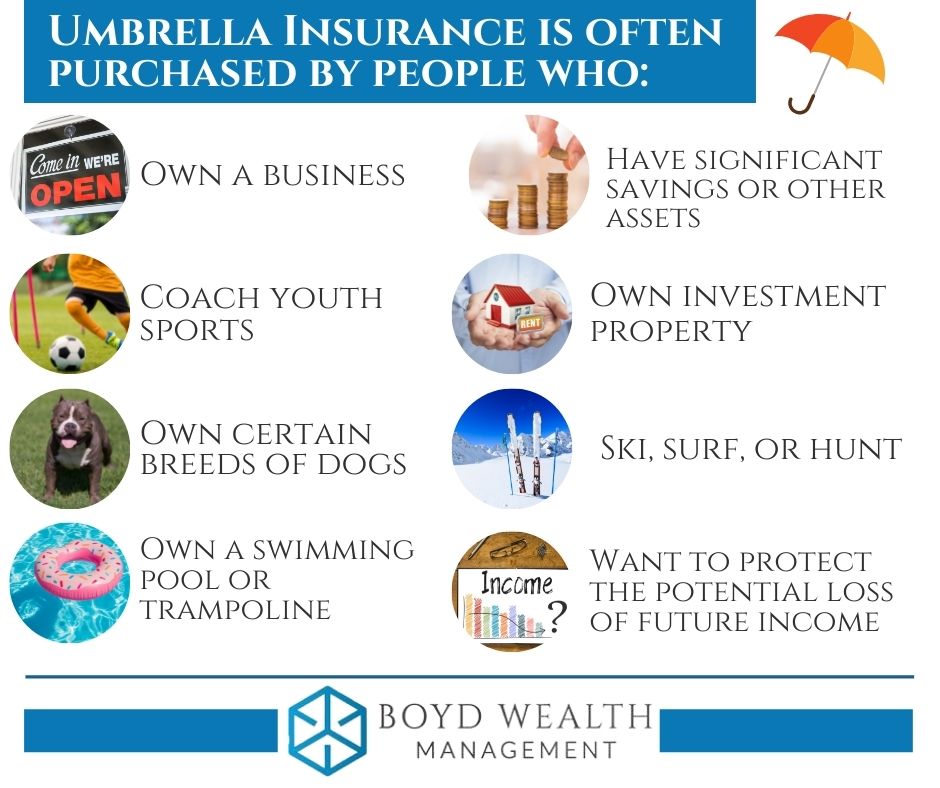

Umbrella Liability

Liability coverage included in home and auto policies are intended to protect you from damages resulting from an auto accident where you’re at fault or someone being injured at your home. However, standard limits are usually not adequate for high-net-worth families. Umbrella policies cover your personal liability in excess of standard home and auto policies.

You will usually be required to carry a minimum amount of liability coverage on your auto policy of $250,000 per person, $500,000 per incident, and $100,000 of property damage. The limit is commonly $300,000 of personal liability for homeowners.

Premiums for umbrella coverage may be more reasonable than you think. According to the Insurance Information Institute, “For about $150 to $300 per year you can buy a $1 million personal umbrella liability policy. The next million will cost about $75, and $50 for every million after that.”

Umbrella insurance typically covers:

• Bodily injury to another person due to a car accident where the policyowner is at fault or an injury to a guest in or around your home.

• Property damage resulting from a car accident

• Personal injury such as slander, libel, false arrest, malicious prosecution, and mental anguish or shock.

Final Considerations

Early in Anthony Kim’s career, it was easy to foresee him rising up the leader board, earning countless tens of millions in a long and lucrative career. The conversation about insuring himself if injury kept him from playing at the highest level may have been unpopular at the time.

Even for the typical investor or high-net-worth family, it’s much more fun to talk about boosting savings, maximizing investment strategies, and reducing taxes. That being said, having a solid risk management and insurance strategy cannot be overlooked.

It’s important to note, I/we are not licensed property and casualty insurance agents. The main role of a Certified Financial Planner™ professional, however, is to look at the big picture and guide discussions.

I hope this conversation spurs a thoughtful discussion with your own agent.

Like most areas of financial planning, there is no one size fits all approach to insurance planning. Each circumstance must be reviewed individually and periodically.

“It’s important for busy, successful people to understand they have exposure. Pull out your policies and ask your agent for a review every couple of years,” adds Kayti Jones.

It’s also worth asking your agent what it might cost to insure your golf swing. It’s probably a lot less than you might think! 😉

Happy Planning,

Brian