Since the early twentieth century, retirees have been advised to shift their portfolios from growth-oriented investments to income-producing ones to compensate for their lost paycheck. Traditionally, this meant investing in bonds, clipping coupons, and using the interest to cover expenses, while largely avoiding stocks.

However, hyperinflation in the 1970s and early 1980s, combined with nearly two decades of near-zero interest rates following the Great Financial Crisis resulted in bond yields that no longer sustained retirees’ spending needs. These economic conditions drove once conservative investors to venture beyond the safety of bonds for more risky stocks.

Publicly traded companies return money to shareholders in two ways: by buying back outstanding shares or paying dividends. Income-focused investors have been particularly interested in the latter, yet there remains a fundamental misunderstanding of how dividends actually work. Specifically, the direct impact returning profits to shareholders has on a company’s stock price.

It is commonly believed that paid dividends are additive to net worth, but this is only true if they are reinvested. Instead, most retirees use dividends as cashflow to supplement their income, resulting in a relentless chase for high yield, regardless of a company’s fundamentals or the industries they represent.

How do dividends work?

When a company pays shareholders a dividend, its assets and share price subsequently decrease to reflect the recent payout. The company may have chosen to distribute a portion of profits, dip into their reserves or even taken on debt to maintain their dividend during an unprofitable time. Regardless, they have less money in their coffers.

For instance, if ABC company, trading at $10 per share announces a $1 dividend, its share price falls to $9 on the ex-dividend date. Due to the dynamism and liquidity of our capital markets, this reduction in valuation can be (and often is) overlooked, but it still exists.

Akin to a bond coupon (interest payment), investors often perceive a dividend as an immediate increase in their wealth. This misconception is known as the free dividend fallacy. Unlike bonds, where investors receive periodic interest payments AND their full principle at the end of the term (assuming no default), dividends are not extra returns on investment. Rather, they represent a forced taxable return of capital, as any “bonus” from dividends is directly offset by the corresponding share price reduction.

Are dividends tax efficient?

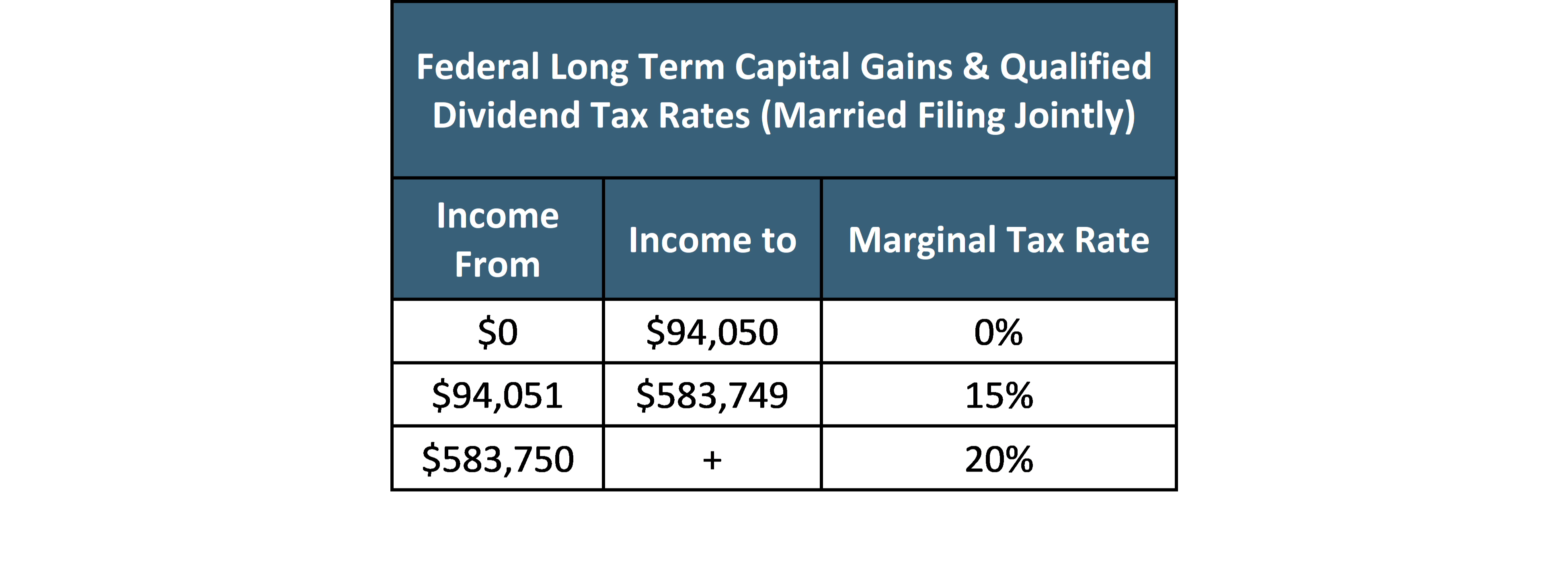

Income-seeking investors often compare the tax treatment of ordinary income of bond payments to qualified dividends from stocks. In this context, dividends are taxed more efficiently. See below:

Yet, comparing stocks and bonds directly is inappropriate. Stocks are inherently more volatile than bonds, which essentially function as loans with a set maturity date and naturally less risk (depending on the borrower).

Yet, comparing stocks and bonds directly is inappropriate. Stocks are inherently more volatile than bonds, which essentially function as loans with a set maturity date and naturally less risk (depending on the borrower).

Instead, retirees relying on their portfolios for cashflow (i.e., do not reinvest their dividends) should compare the tax implications of dividend-paying stocks to their non-dividend paying counterparts, which retain earnings for growth or buy backs. An investor that spends their scheduled divided payments versus one that creates “homemade” dividends by selling stocks, thereby generating capital gains (or losses), can generally expect similar marginal tax outcomes:

However, manually generating homemade dividends provides more flexibility, allowing an investor to select specific positions and tax lots to sell, potentially realizing capital losses to offset capital gains or even directly reducing taxable income (by $3,000 in 2024). Additionally, it prevents forced realization of taxable income when distributions are unnecessary, enabling investors to align income more closely with their spending needs.

Are companies that pay dividends in good shape?

While some great companies consistently pay and increase their dividends, the payments are not always indictive of a robust balance sheet. Many companies pay dividends despite operating at a short-term loss and CEOs may prioritize these payments to support their share prices, even borrowing money to maintain them. Few impediments exist to prevent unhealthy, weak businesses from doing so. Lastly, constantly returning funds to shareholders may signal a company views this as a better use of their capital than reinvesting in themselves or pursuing innovation, potentially widening the gap between such companies and high-flying growth firms.

Furthermore, dividend driven portfolios tend to be concentrated in old economy sectors, such as financials, utilities and energy. This lack of diversity can be especially detrimental during volatility or market downturns.

Though dividends and companies that pay them are pitched as reliable hedges against market uncertainty, their share prices are not immune to drawdowns, and their dividends can be cut when investors rely on them most.

For example, in 2020 as Covid-19 led to global lockdowns, companies strapped for cash cut an estimated $220 billion in dividends globally. Central banks limited or barred banks and other financial institutions from paying dividends until their balance sheets were fortified and the risks of bank runs ruled out. Royal Dutch Shell cut its dividend (by 66%) for the first time since 1945. All the while there was significant pressure on their share prices.

Dividend cuts are not exclusive to crises, as we have seen big name firms like Rolls Royce and ConocoPhillips slash their payouts in the middle of the bull market in 2016, demonstrating that dividends are not guaranteed.

Bottom Line

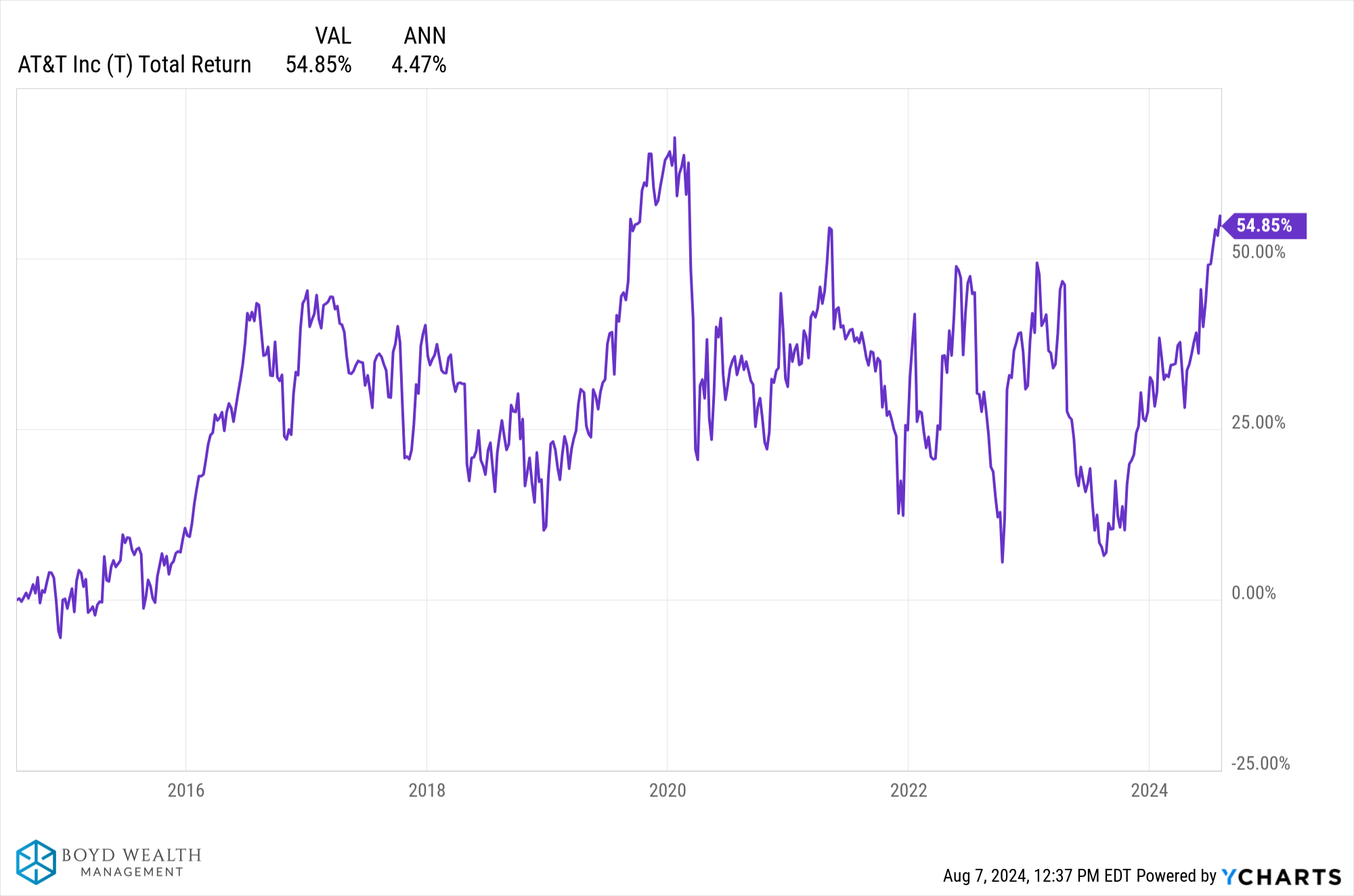

Reinvested dividends account for a significant portion of compounded market returns since the 1960s (BWM's Power of Dividends article). Despite this, many retirees elect to spend their dividends rather than reinvest them. As an example, AT&T has returned 4.47%/year the past decade, assuming all earnings were reinvested. See chart below:

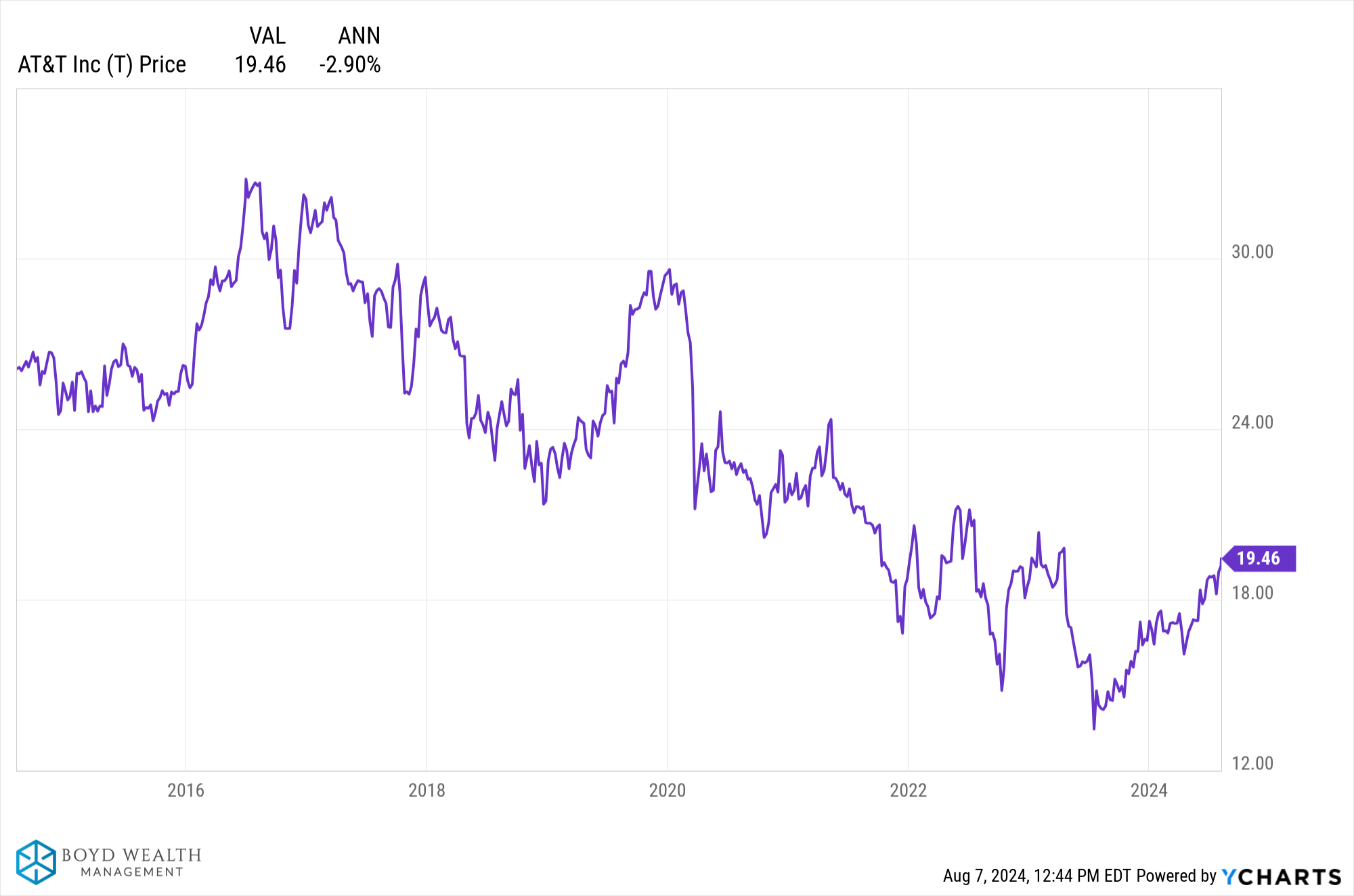

In contrast, an investor in AT&T who spent all their dividends would have seen the value of their position decrease 2.90%/year in the same time period:

As the old saying goes, “there is no free lunch in investing” and dividends are no exception. If investors better understood the free dividend fallacy - the direct relationship between a company’s share price and paid dividends - they would be less dazzled by companies boasting unsustainable dividend yields (i.e., AT&T), nor use dividends as a driving force for investment decisions.

Instead, investors should consider a diversified total return approach, in which reinvested dividends, interest and price appreciation (capital gains) collectively drive returns. This strategy prevents limiting investments to dividend payers as over 60% of domestic companies do not pay them, and includes fast growing ones that spearhead innovation and often buy back shares to boost price appreciation.

If income is needed, investors can simply generate their own “dividends” in a tax efficient manner, preventing the forced receipt of taxable distributions associated with scheduled dividends.

Though many investors feel differently about receiving dividends versus manually selling holdings, both generate income, and a dollar is a dollar regardless of how it is obtained. Therefore, retirees should avoid narrowing their investment options (i.e., chasing yield) and strive for a portfolio that maximizes the chances of achieving their financial objectives.

Colby

For more information on how we can assist with your wealth planning, you can schedule a 30-minute introductory call here. Our team of professionals are dedicated to providing tailored solutions that align with your financial objectives.

Sources/Further reading:

- Swedroe, L. & Berkin, A. (2020). The Incredible Shrinking Alpha: Harriman House.

- https://www.reuters.com/plus/fisher-investments-on-why-dividend-stocks-magic-is-a-myth

- https://impactadvisorsgroup.com/how-dividend-stocks-work/