The 2010s passed by at warp-speed. Only in retrospect can we now see it was an incredible decade for investors.

We just completed our 12th annual Economic Outlook Breakfast at Del Paso Country Club and were privileged to present a very special guest Omar Aguilar, Chief Investment Officer of Charles Schwab Investment Management. More on Omar and his outlook in just a moment.

Asset Class Returns Quilt for 2020

There’s so much noise if you look at an investment portfolio on a daily, weekly, or even monthly basis. But when you look back over a year, and especially a decade, it can provide real perspective.

We’ve updated our most requested piece, our Asset Returns Quilt for 2020, which you can view and download here:

2020 Asset Class Returns Quilt - BWM.pdf

Highlights of 2010s

- The 2010s were the only decade in modern history – basically since the Civil War - without a recession in the US.

- We currently find ourselves in the 126th month of economic expansion, which is the longest expansion in modern history.

- The S&P 500 (the largest stocks in the US) climbed throughout despite experiencing 6 drawdowns greater than 10%1.

We were once again reminded that drawdowns are normal, they’re usually very scary in the middle, and always appear to be permanent.

These drops are a feature, not a bug. Volatility shakes out the weaker hands. As I’ve said before, it’s surviving these drawdowns (risk) that ultimately provides the upside (returns).

In spite of these normal drawdowns, US stocks grew remarkably over the previous 10 years.

- From an investment standpoint, it was the decade no one wanted to end. Isn’t that how most incredible journeys go? Twists and turns, highs and lows, unpredictable outcomes.

- 9 out of those 10 years were positive for US stocks which delivered an average annual return of 13.1%.

- It was not the best performing decade, believe it or not. In fact, both the 1980s and 1990s saw 9 out of 10 positive years with returns averaging 17.3% per year in the 80s and 18% in the 90s2.

- Unemployment sits at a 50-year low of 3.5%.

- And while it’s been the longest expansion, it’s also been the weakest in terms of GDP growth. Frankly, it felt like even though the stock market climbed, and the economy grew, no one was ever all that happy about it.

In our blog post “Recession Talk is Building – Here’s Your Game Plan” from October 22nd we wrote, “Perhaps it’s this expectation that the other shoe could drop any minute that's kept the party going for so long.”

Where do we go from here? It’s difficult to imagine a repeat of the last decade, but you do have a President that watches the stock market intently.

In case you missed it, this tweet made me chuckle. First, I’m not sure he’s ever participated in a 401(k) as it’s hard to believe this was a typo with the 1 and 9 nowhere near each other on the keyboard. Second, he’s shouting out returns with no clear timeframe or index and then taunts investors who may have “only” achieved 50% returns.

The tweet was subsequently deleted and then reposted with only “401(k)” being corrected. The taunting was left unchanged.

Omar Aguilar, PhD

Perhaps you’ve seen him quoted in financial publications or you recognize him from his regular appearances on CNBC.

Omar Aguilar is Senior Vice President and Chief Investment Officer of Equities and Multi-asset Strategies for Charles Schwab Investment Management.

What makes Omar so unique is his extensive knowledge of both economics and human behavior. He received a bachelor’s degree in Actuarial Sciences and a graduate degree in Applied Statistics from the Mexican Autonomous Institute of Technology (ITAM). Then, he was a Fulbright Scholar at Duke University’s Institute of Statistics and Decision Sciences, where he earned a Masters of Science and doctorate degrees.

With more than 20 years of broad investment management experience in equity markets, Omar currently oversees $235 billion in assets at Charles Schwab.

He discussed the current macroeconomic environment while also shining a light on the behavioral biases that all investors grapple with when making decisions about their money. He demonstrated how identifying those biases and having a plan to combat them can help investors achieve better financial outcomes.

Behavior

Emotional and Cognitive Biases effect investors ability to make successful decisions with their money. Omar discussed a few in the context of investor behavior.

- Recency Bias: This is the tendency of humans to over extrapolate the recent past or present into the future. Said another way, assuming the future will be the same as it is now.

It was extremely difficult for investors to foresee US stocks returning 31.49% in 2019. Markets dropped 20% at the end of 2018 and there was so much discussion of slowing economic growth and recession. Unchecked, an investor acting on recency bias would have sold out of their positions and run for cover at the end of 2018.

- Loss Aversion: It’s been scientifically proven that humans feel the emotional jolt of a loss twice as much as they experience joy from a gain. This causes investors to sell winning positions too soon or to sell losing investments at the bottom of normal cycles.

- Confirmation Bias: This is the tendency to ignore information contrary to your point of view or interpret all information in a manner favorable to your point of view.

Who hasn’t been guilty of this? How many of us only read publications, watch channels, or follow those on social media that support our own opinions?

While extremely difficult in practice, it’s important to periodically listen to those points of view you don’t necessarily agree with. For us, it’s being open to the opinions of doomsdayers even if history and current economics aren’t on their side.

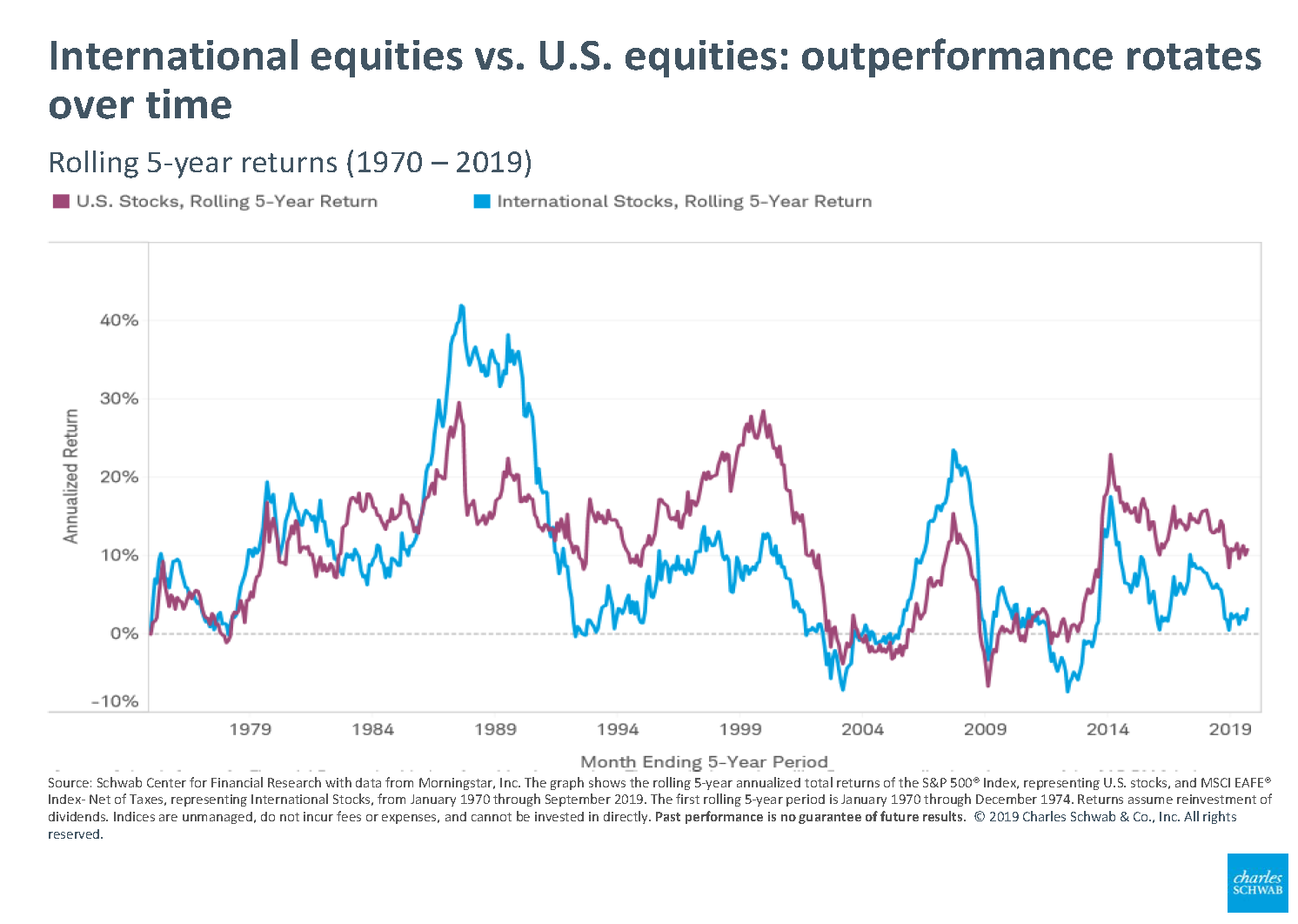

Omar pointed out how the outperformance of US stocks versus International stocks over the last decade has caused many investors to abandon International Stocks even though they make up 45% of worldwide global equity market.

Taking a step back reveals that leadership between US stocks and International stocks have alternated since the 1970s. Owning both as part of a diversified portfolio should continue to provide valuable diversification benefits in the future.

What’s in Store for the 2020s?

Omar and his team are some of the best and brightest minds in the industry. Great economists review multiple current data points, review in a historical context, and attempt to extrapolate to an uncertain future.

What is the current data telling us?

Economics

- Omar and his team believe that a new decade brings slower economic growth.

- Consumer spending and a tight labor market will sustain economic growth while central banks which are both dovish and “flexible” will continue to be accommodative.

- China economic activity is improving, particularly with a Phase 1 trade deal signed and the potential for fiscal stimulus to kick start growth in Europe. There is a risk in the short run of a temporary slow-down due to the onset of the new coronavirus.

Fundamentals

- Improving monetary, liquidity, and credit conditions continue to boost risk assets such as stocks and real estate.

- Earnings growth could resume alongside accelerating economic growth.

Valuation

- Multiple expansion in equities likely continues. In a low interest rate environment, investors are typically willing to pay more for a stock per dollar of company earnings. As long as rates remain low, investors find themselves in a world of TINA – There Is No Alternative.

- The yield on cash in money markets and online banks is currently around 1.70%3.

- The yield on a 10-year treasury around 1.60%4.

- The yield on the S&P 500 ETF (SPY) is currently 1.65% with the upside potential of stock price appreciation5.

- The yield on the International Developed stock ETF (EFA) is currently 3.4% with the upside potential of stock price appreciation5.

There is more volatility inherent in stocks but also more return potential relative to cash and government bonds. With inflation around 2%, this could continue to make stocks attractive causing higher multiples.

Sentiment

- The easing of trade tensions supports investor confidence

- Transition to relatively inexpensive cyclical sector. Growth stocks, led by Big Tech, have outperformed value stocks over the last decade. They have historically swapped leadership and we may see the shift to value this year and into the decade.

Key Takeaways

The key to combating behavioral biases, particularly as it relates to financial decisions, is to develop a disciplined rules-based plan. This removes human emotion from the decision-making process.

With our portfolio return expectations muted over the next decade, it’s clear the winners will be those with a disciplined investment strategy, a disciplined withdrawal strategy for generating retirement income, and a disciplined strategy to grow and preserve wealth despite short-term market fluctuations.

Warren Buffet said, “It’s only when the tide goes out that you learn who has been swimming naked.” In a ten-year bull market, many investors did well over the last decade without an accurate understanding of their risk.

There are many individual investors and advisors that have once again abandoned asset allocation. In turn, they have loading up on Big Tech, neglected International Equities, and may be taking on more risk than they want or understand. Many portfolios are still expensive and tax inefficient.

These are the things that only come to light “when the tide goes out.”

If you’re not a client and it’s been a while since you’ve reviewed your asset allocation or portfolio risk, feel free to reach out to see how we can help.

Cheers to a healthy, happy, and prosperous 2020!

Happy Planning,

Brian

Further Reading/Resources

1. Data from Koyfin

2. Fortune Magazine – Ben Carlson

3. Bankrate – Best Online Savings Accounts Jan 2020

4. Data from CNBC as of January 30th, 2020

5. Data from Koyfin