We’re closing in on the end of another incredible year for stocks.

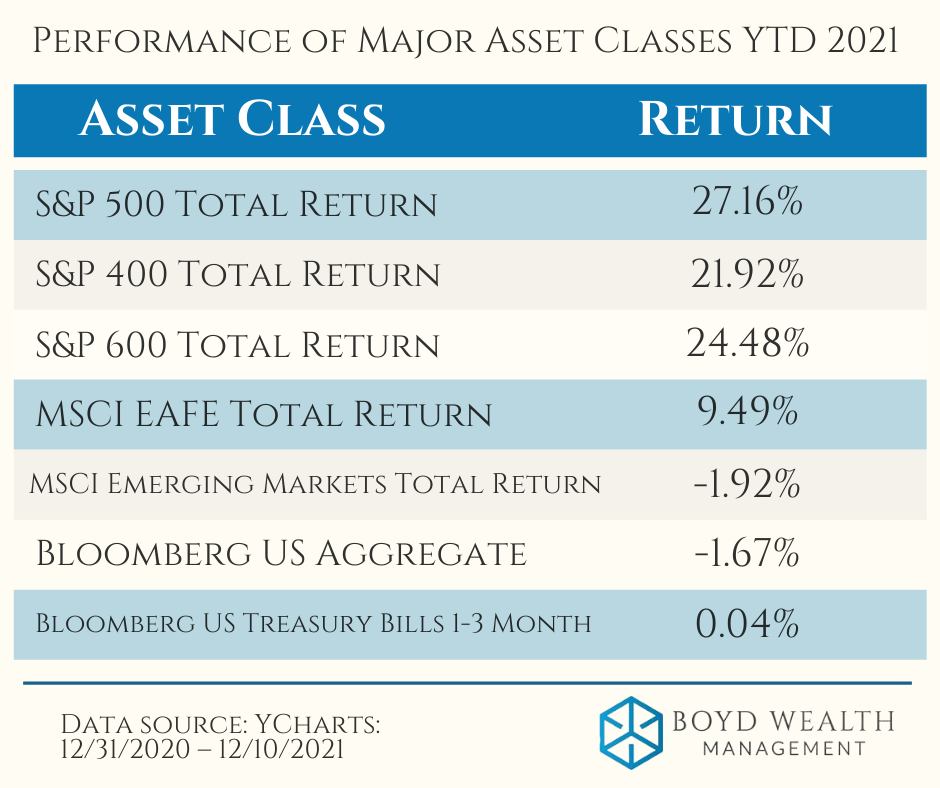

US Large Cap Stocks (S&P 500) are leading the way again 2021, with Mid Cap (S&P 400) and Small Cap Stocks (S&P 600) trailing close behind. International Developed Markets (EAFE) are having a good year as well.

Laggards this year include Bonds (Bloomberg Agg) and Emerging Market Stocks.

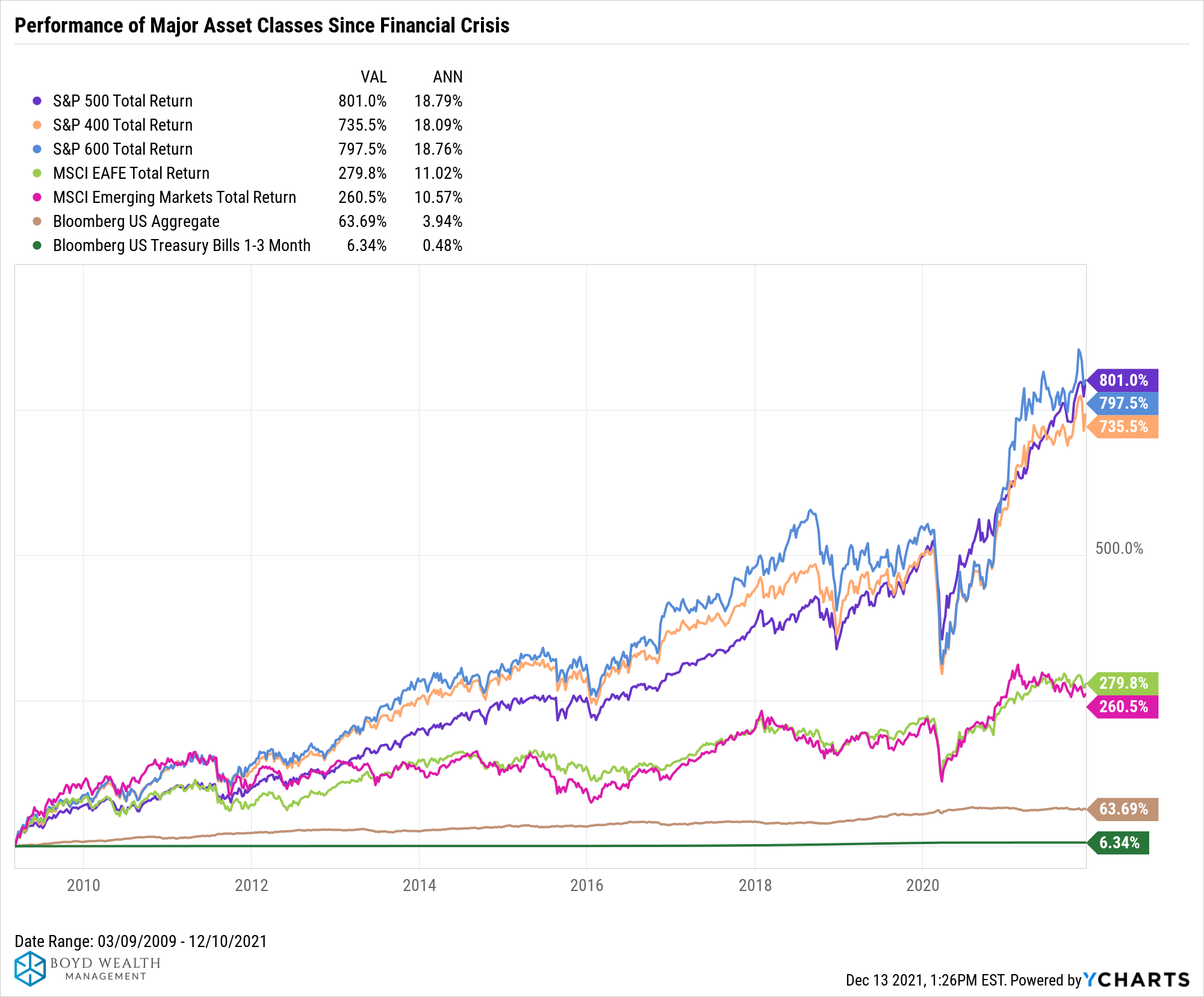

In fact, 2021 is the continuation of an incredible run for stocks, producing impressive returns since the market bottomed during the financial crisis in 2009. Fueled by loose monetary policy (low rates), with moderate yet consistent economic growth, stocks have ground their way higher for more than a decade.

Since March 9th, 2009, the S&P 500 has averaged an incredible 18.79%. That mark significantly surpasses the 10.6% average annual return of the S&P 500 going back to 1990.

With this profound run of success, individual investors’ expectations for future returns have increased accordingly. Financial professionals are seeing things a bit differently, however.

In a recent study, Natixis Investment Management surveyed 8,550 investors across 24 countries.

They found that individual investors expect an average long-term return of 14.5% above the rate of inflation. Financial professionals, however, expect only 5.3% above inflations – a wide chasm.

Source: Natixis Investment Management, 2021 Individual Investor Report, “The Next Normal: Are investors prepared for the post-Covid markets?”

There are a few strong variables that are leading financial professionals toward projecting muted returns over the next decade.

The first variable is the concept of “reversion to the mean”. In lay terms, returns tend to cluster toward a long-term trend with any large sample size. So, if the historical average of the market has been roughly 10% and we’ve recently experienced 18%, it’s safe to assume future returns will move us back toward that average.

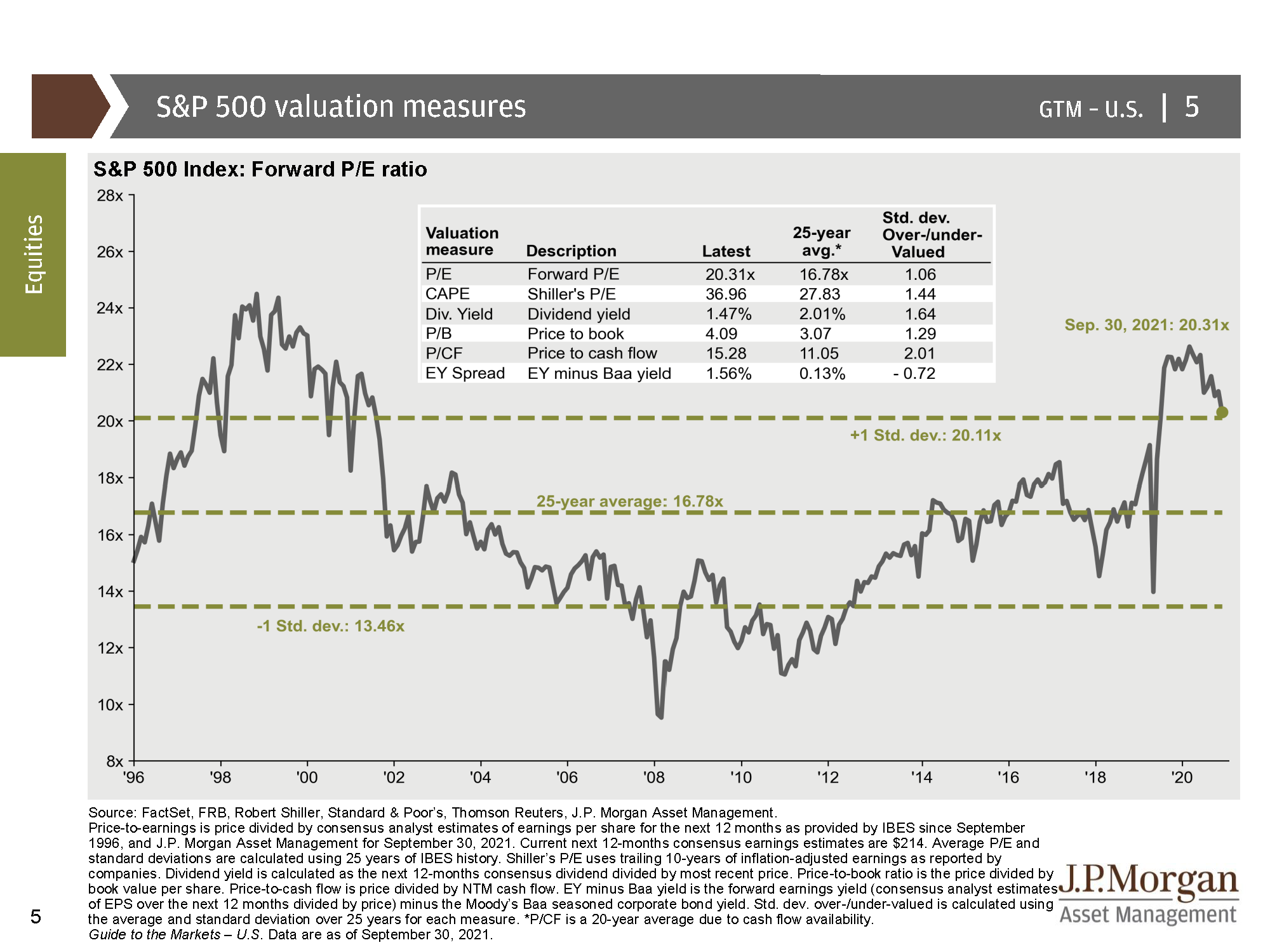

The second is both higher (although not extreme) current equity valuations and low interest rates. Future returns for stocks have generally been lower when starting from current valuations. One preferred measure of valuations is the Price-to-Earnings ratio (P/E ratio), a measure of how much an investor is willing to pay for a stock in exchange for $1 of earnings.

While the current valuation for the S&P 500 is not extreme, at 20.31x it is elevated relative to history.

Low rates have pushed many investors and institutions toward equities as yields from bonds and cash equivalents have been unattractive. The acronym of the 2010s was TINA – There is No Alternative.

Current bond yields are also a pretty good predictor of future bond returns. With the 10-year treasury yielding approximately 1.5%, it’s reasonable to expect the 10-year total return on those bonds to be close to 1.5%. Corporate bond yields are currently 2.67%1.

In their December release, you can see expected future returns across asset classes from Vanguard:

To summarize, US stocks are projected to return between 2.3% and 4.3% per year.

International and emerging markets stocks come in slightly better at between 4.2% and 7.3%.

Bonds are expected to deliver between 1.4% and 2.4% per year.

Vanguard is not alone in their thinking. In fact, a chorus of investment firms project lower returns ahead. Investors would be well-served to prepare for that probability.

We referenced a similar chart in our recent Social Security Guide where we briefly discussed the importance returns can have on claiming strategies.

Using Vanguard’s mid-point numbers, the classic US 60%/40% stock-to-bond portfolio is projected to return between 2%-3.5% per year. Of course, the aim is to improve on that using a globally diversified portfolio.

So, what are investors to do?

1. Reset Expectations

It’s not like investing has been easy over the last decade. On the contrary, investors had to climb an incredible wall of worry to earn those outsized returns. Still, during that period, the market pushed sharply higher for those willing to pay the price of admission – patience through periods of intense volatility. That kind of patience and discipline will come in handy as you prepare for the next decade, which may feel more like a slog.

The expectation of lower returns is not new. In fact, over the last 5 years, we’ve been using conservative return assumptions in your financial plans, testing outcomes to this potential reality. So far, we’ve been blissfully wrong. But it’s better to plan for lower returns and exceed those expectations than use higher returns and underperform.

Moreover, when faced with an uncertain multifaceted world economy, it’s best to focus on the things you can control - how much spend, how much you save, and the amount of portfolio risk you take on.

*J.P. Morgan Guide to Retirement 2021, p.3

2. Minimize Taxes and Fees

Taxes and fees are two large detractors from investment portfolio returns. One way to minimize both is to use exchange traded funds (EFTs) where possible (especially in taxable accounts). ETFs produce very little turnover (taxes) and come with a very low cost.

For reference, the cost of the Vanguard S&P 500 ETF is a microscopic .03% per year. When I started investing and advising, the average cost of a good actively managed US mutual fund was north of 1% per year.

Actively managed stock mutual funds typically cost more, generate more realized capital gains, and are statistically more likely to underperform their index benchmarks over the long run.

Another way to minimize the impact of taxes is through tax-loss harvesting. We’ve written about this strategy and actively deploy it in your portfolios. Essentially, we’re looking for opportunities to take paper losses on holdings that have temporarily lost value. We then purchase a materially different security with exposure to a similar sector of the market and reset cost basis. Losses can then be used to immediately offset gains elsewhere in the portfolio or can be banked to offset gains in future years.

3. Use Active Portfolio Management

Dynamic asset allocation strategies are those that make changes to their asset or risk allocations within certain well-defined parameters. This allows for active adjustments based on changing market and economic conditions. Typically used as a risk management tool and to help manage investor behavior, the goal is to improving risk-adjusted performance over time.

Given the potential for lower future returns, we use quantitative data to inform the asset allocation of our portfolios. Portfolio models are still built with the same core building blocks – diversification and risk management. But layered on top is a rigid, disciplined framework to tilt the portfolio’s holdings based on current data, all while staying within one’s risk tolerance.

We don’t use this data to make all-in or all-out market timing decisions, which have proven disastrous for returns. Instead, we use hard data to make statistically relevant decisions with the goal of improving returns and minimizing risk through a full market cycle.

The Bottom Line

Making any kind of predictions about the future, including return assumptions, is an imperfect science. It’s impossible to predict the multitude of variables that influence the global economy, central bank policy, interest rates, inflation, corporate profit margins, and investor psyche, just to name a few.

While I do hope stock market returns over the next decade mirror the last, I recognize that hope is not a sound strategy.

Therefore, we’re here with you every step of the way, helping set correct expectations while actively monitoring your financial plan and portfolios.

We’ll have more to report at our annual Economic Outlook Breakfast on January 19th at Del Paso Country Club. We’re even bringing back special guest and “quant-nerd” Chris Shuba from Helios Quantitative Research to enlighten us all.

Look out for an email invitation in the next week or so.

Until then, we’re wishing you the best this Holiday Season!

Happy Planning,

Brian

*Boyd Wealth Management, LLC is a registered investment adviser. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and, unless otherwise stated, are not guaranteed. Be sure to first consult with a qualified financial adviser and/or tax professional before implementing any strategy discussed herein. Past performance is not indicative of future performance.

Sources/Further Reading:

1. Moody's Seasoned Aaa Corporate Bond Yield, 2.67% for Dec. 10, 2021, YCharts

Blackrock Long-Term Capital Market Assumptions

2022 J.P. Morgan Asset Management Long-Term Capital Market Assumptions