When considering the sale of your business, buyers will almost always approach the transaction with priorities that differ from yours. Buyers generally have a preference to purchase assets, while sellers typically favor stock sales. These competing objectives often lead to lengthy negotiations over the ultimate purchase price of your business, the structure of the deal, and, potentially, earnouts.

Conventional wisdom says sellers should push for a stock sale and avoid asset sales when possible due to unfavorable tax treatment. However, for asset-light businesses, such as software companies or professional services firms, an asset sale can actually produce better after-tax outcomes than a stock sale.

Below, I’ll discuss the differences between stock and asset sales and explain how business owners of pass-through entities (e.g., S-Corps and Partnerships) living in states with high income tax may be able to increase the purchase price of their business, while reducing taxes by exiting through an asset sale.

The Basics

What is a Stock Sale?

In a stock sale, the buyer acquires ownership interests in the seller’s business, assuming all the assets, such as accounts receivable, inventory, and intellectual property, and the liabilities, such as environmental exposures, employee-related claims, and unpaid taxes, whether known or unknown.

Stock sales are often simpler from an administrative perspective. Contracts with vendors, customers and employees continue as-is and generally don’t need to be redone, limiting operational friction for the buyer.

That said, there are material disadvantages for the buyer in a stock sale, specifically relating to taxes. When purchasing a company’s stock, the buyer assumes the seller’s existing tax basis in the assets. Meaning, if the seller fully depreciated the acquired tangible assets (e.g., equipment, machinery, etc.) the buyer cannot depreciate the assets further, limiting how much they’re able to reduce taxable income. Similarly, key intangible assets that often drive the value of a business, such as the client list and seller’s goodwill, are not amortizable over a 15-year period in a stock sale, as they are in an asset sale (more on this later).

From the seller’s perspective, stock sales are clean and often more tax advantageous than asset sales, particularly for businesses with significant, fully depreciated tangible assets. Rather than triggering depreciation recapture, which can be taxed up to 37% federally, stock sale proceeds are generally taxed at preferential capital gain rates, up to 20% federally (subject to a 1 year holding period requirement).

Buyers frequently address this tension between operational efficiency and tax inefficiency of a stock sale through a 338(h)(10) election or an F-Reorganization. While F-Reorgs have become more common in recent years, both structures generally achieve the same outcome for the buyer. The transaction is treated as a stock sale for legal purposes, but as an asset sale for tax purposes. This enables the buyer to continue operating the target company without interruption, while depreciating the acquired assets (thereby reducing taxable income) since the seller’s low tax basis is not carried over. Given their complexity, legal counsel should be involved if either election is proposed by a buyer.

What is an Asset Sale?

In an asset sale, buyers selectively pick which assets of the target company they’d like to acquire and leave behind any unwanted assets and liabilities. Following the transaction, the selling company continues to exist as a legal entity and retains the assets and liabilities not transferred or assumed in the transaction.

Not only does an asset sale limit the buyer’s liability, they’re also extremely tax advantageous. Rather than assuming the seller’s tax basis of the acquired assets like in a stock sale, the buyer’s tax basis is stepped up to the purchase price of each asset (i.e., fair market value). This effectively resets the “depreciation clock” for the acquired assets, allowing the buyer to significantly reduce their taxable income.

The tax benefits of an asset sale are even more noteworthy since the One Big Beautiful Bill Act (OBBBA), signed into law on July 4th, 2025, made 100% bonus depreciation permanent. Now, buyers can fully expense qualifying tangible assets the first year they’re placed into service. Intangible assets can also be expensed but they’re amortized over 15 years rather than a single year.

For sellers, tax treatment depends on the type of asset sold. Tangible assets, such as inventory and depreciated equipment or machinery, will generally be taxed as ordinary income, with federal rates as high as 37%. While intangible assets are taxed at more favorable long-term capital gain rates, capped at 20% federally. Given this 17% difference in tax rates, sellers are incentivized to allocate as much value as they can substantiate to intangible assets during deliberations.

For asset-light businesses with very little tangible assets, most of the purchase price will be allocated to the client list, goodwill, and non-compete agreements (if there are any). Given these assets are taxed more favorably than ordinary income, the initial tax treatment of an asset sale closely resembles that of a stock sale.

Notably, while asset sales can sometimes be less favorable for sellers from a tax perspective, buyers greatly benefit from the limited liability and tax advantages. As a result, asset sales can command a higher purchase price. This adjustment to the purchase price, known as a “gross-up”, can help sellers offset the potential tax disadvantages of an asset sale.

So Why Might an Asset Sale Be Better Than a Stock Sale?

If both transaction types result in primarily long-term capital gains for an asset-light business, why should an owner prefer an asset sale?

The answer lies in the interaction between the State and Local Tax (SALT) deduction cap and the Pass-Through Entity Tax (PTET).

SALT Cap and PTET

The 2017 Tax Cuts and Jobs Act (TCJA) limited taxpayers’ ability to deduct up to only $10,000 of SALT (e.g., income tax, general sales tax and property tax) from their federal income. The 2025 OBBBA subsequently extended the federal SALT deduction limitation through 2029, but raised the cap to $40,000, with a 1% annual inflation adjustment (i.e., $40,400 in 2026) through 2029, for taxpayers that make less than $500,000.

In response to the deduction limit, high income tax states, such as California, introduced a workaround for owners of pass-through entities (e.g., S-Corporations and Partnerships), which is now known as the Pass-Through Entity Tax (PTET).

Rather than paying state income taxes personally, and being subject to the SALT limit, pass-through businesses in California can elect to pay a 9.3% tax on qualifying business income at the entity level. By doing so, the tax payment (“PTET payment”) is treated as a deductible business expense, reducing the entity’s net income that ultimately “passes through” to the owner’s personal federal tax return.

What does PTET have to do with selling a business?

PTET can materially affect the taxation of a business sale because stock and asset sales are treated differently for purposes of determining business income. In short, proceeds from stock sales are not qualifying business income, therefore PTET payments are not permitted. While proceeds from asset sales are qualifying business income, so PTET payments are permitted. Meaning, businesses whose purchase price is primarily allocated to intangible assets and taxed as long-term capital gains, are likely to significantly reduce their federal tax liability in an asset sale rather than a stock sale.

Let’s look at an example.

Example

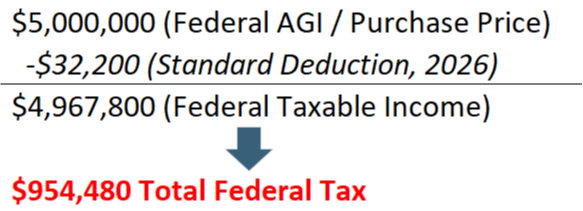

Stock Sale (No PTET Payment)

Because the taxpayer’s income exceeds $500,000, their federal SALT deduction is limited to $10,000, despite having paid significantly more in state income taxes. Given the SALT deduction limit, many high earners no longer have sufficient deductions to itemize and instead default to the standard deduction, as illustrated in this example.

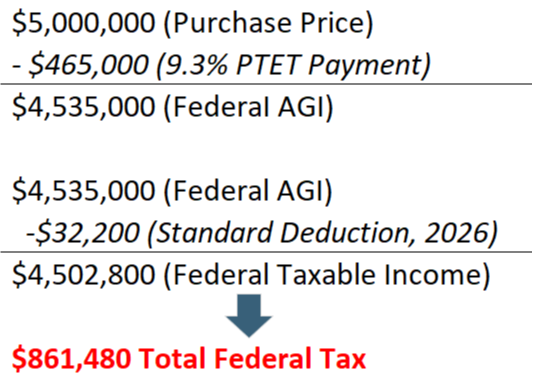

Asset Sale (With PTET Payment)

By paying state taxes at the entity level, the owner bypasses the federal SALT cap, while still claiming the standard deduction, resulting in a meaningful reduction in their federal tax liability.

Bottom Line

During negotiations, it should not be assumed that a stock sale will produce the most favorable tax outcomes, particularly if you live in a state with high income taxes. Given the ability to bypass the federal SALT deduction limit by making a PTET payment, asset sales, in many cases, are likely to result in superior after-tax outcomes for owners of asset-light, pass-through businesses, despite conventional wisdom.

Selling a business you’ve built from the ground up is rarely straightforward, and doing it well requires thoughtful planning before negotiations begin. So, if you’re considering a sale in the next 1-3 years, now is the time to model asset vs stock sale scenarios, and evaluate PTET eligibility, well before signing an LOI. The right planning done early can materially change the economics of your exit. After all, it’s not about what you sell the business for, it’s about what you keep after accounting for taxes.

We frequently help business owners prepare for their exit and plan for life after the sale. If you have questions about this process, please feel free to reach out.