You’ve probably heard the term “Mega Backdoor Roth” mentioned before but aren’t quite sure exactly what it means or whether it’s a strategy worth considering. In our experience, many employer sponsored retirement plans don’t support the transactions needed to complete a Mega Backdoor Roth, largely due to IRS nondiscrimination rules.

That said, for those whose retirement plans do permit these transactions, and are looking for ways to save beyond the standard 401(k) contribution limits, the Mega Backdoor Roth can be a powerful strategy. When done correctly, it can meaningfully increase tax-free retirement savings. Here’s how it works.

Requirements

Before diving into the details, it’s important to note the requirements needed to complete a Mega Backdoor Roth. Your 401(k) plan must offer both of the following features:

1. After‑Tax Contributions Beyond the Standard Contribution Limits

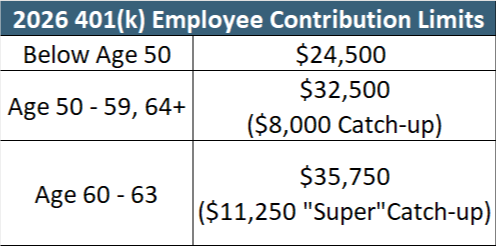

After-tax contributions are deferrals that you make into your qualified retirement account beyond the standard contribution limits set by the IRS seen in the table below:

Many small to mid‑sized companies don’t offer this feature due to nondiscrimination testing. Simply put, the IRS requires that 401(k) plans don’t disproportionately benefit highly compensated employees (HCEs). While safe harbor contributions help retirement plans satisfy these rules by ensuring eligible participants benefit regardless of compensation, they do not apply to after-tax contributions, which are tested separately.

Since after-tax contributions generally only appeal to high earners with strong cashflow, a plan can fail its testing if mostly highly compensated employees are making them. When this happens, the plan can be forced to refund contributions back to the high earners. Something nobody wants. Given this risk, many small to mid-sized plans don’t allow after‑tax contributions.

Ultimately, the demographics of a retirement plan make a big difference. Owner-only plans or plans composed primarily of highly compensated employees are often well-suited to allow after-tax contributions without failing testing, which we’ve commonly seen in the tech industry.

If testing rules prevent owners or highly compensated employees from completing a true Mega Backdoor Roth, an alternative is to convert employer contributions (e.g., matching or profit-sharing) to Roth. While not a perfect substitute, it can achieve a similar outcome: savings in a Roth-style account that ultimately benefits from long-term, tax-free growth.

2. In-Plan Roth Conversions

If your plan allows after‑tax contributions, the next requirement is the ability to convert those after-tax dollars immediately to the Roth “bucket” of your 401(k). Since you don’t receive an income deduction and already paid tax on the dollars contributed (hence “after-tax”), converting them to Roth isn’t a taxable event.

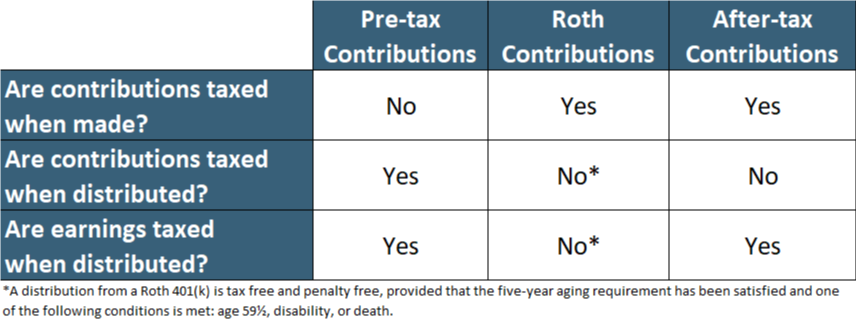

This step is critical because if your retirement plan or recordkeeper (think John Hancock, Fidelity, Empower, etc.) doesn’t permit Roth conversions, the after-tax contributions remain in a pre-tax “bucket” of the 401(k). While the after-tax contributions are treated as basis (i.e., non-deductible contributions) and are not taxed again when withdrawn or converted, any future growth/earnings on those contributions will be taxable when distributed or converted. See table below:

That’s why immediately converting the after-tax funds to Roth, before meaningful growth occurs on the contribution, is key.

If your plan and/or recordkeeper allows after-tax contributions but does not allow in-plan Roth conversions (or in-service distributions to a Roth IRA), you won’t be able to execute a true Mega Backdoor Roth. You’ll still benefit from the ability to save additional dollars in your retirement plan but will miss out on the tax-free growth that makes the Mega Backdoor Roth strategy so powerful.

For example, we know of certain recordkeepers who don’t offer in-plan Roth conversion functionality. Therefore, fully completing this strategy would require the plan document to permit in-service distributions, allowing after-tax contributions to be rolled into a Roth IRA outside of the 401(k). A complex process that involves many steps.

What is the Mega Backdoor Roth?

Now that we understand the two requirements, let’s review the mechanics of this strategy.

The Mega Backdoor Roth is a two-step process:

- Make an after-tax / non-deductible 401(k) contribution beyond the standard limits set by the IRS

- Immediately convert those dollars to Roth 401(k) (or a Roth IRA if the plan allows for in-service distributions)

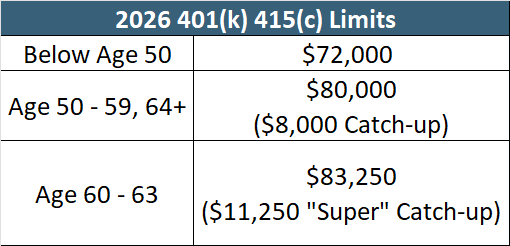

To determine how much after-tax money you can add to your 401(k) in a given year, you must review the Internal Revenue Code’s section 415(c), which sets the annual limit on total contributions for qualified retirement plans. See below:

The 415(c) limits include ALL contributions:

- Your employee deferrals

- Employer match

- Employer profit‑sharing

- After‑tax contributions

So, the amount you can contribute on an after‑tax basis is the difference between your combined employee and employer contributions (deferrals, match, and profit‑sharing) and the 415(c) limits shown above. Let’s look at a couple examples.

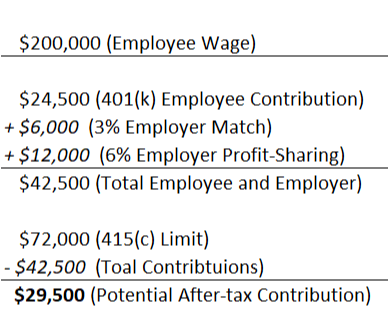

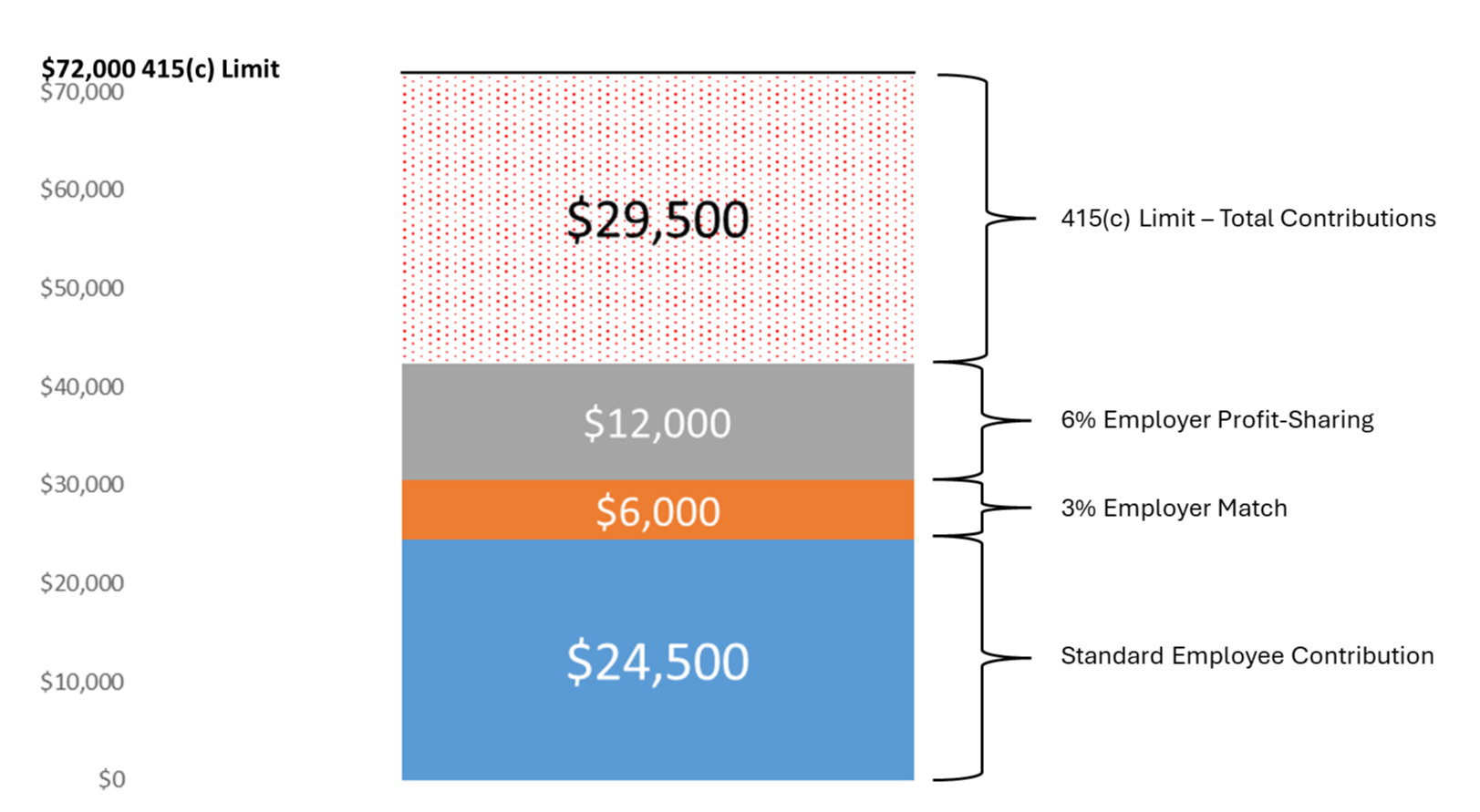

Example 1:

A 40-year-old earning $200,000, maxing out employee deferrals, with a 3% employer match and 6% employer profit-sharing:

In this instance, assuming the plan allowed it, this individual could make a $29,500 after-tax contribution to their 401(k).

One important consideration is that if this individual maximizes their after-tax contributions and reaches the $72,000 415(c) limit, they could reduce their potential for additional employer profit-sharing. For example, if the employer has a strong year and wants to allocate more than a 6% profit-sharing contribution, this individual’s retirement account would not be eligible for the additional amount because they’ve already reached their annual limit. While it can be uncommon for employers to adjust profit-sharing percentages, planning for after-tax contributions can be tricky because employee deferrals must be in the system by December 31st of the plan year, while profit-sharing isn’t determined until the following year when the business files its taxes.

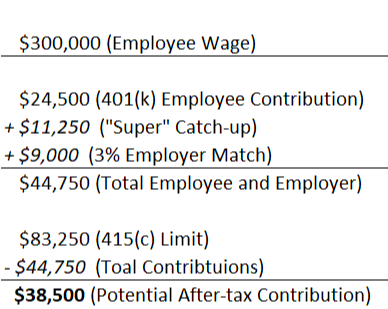

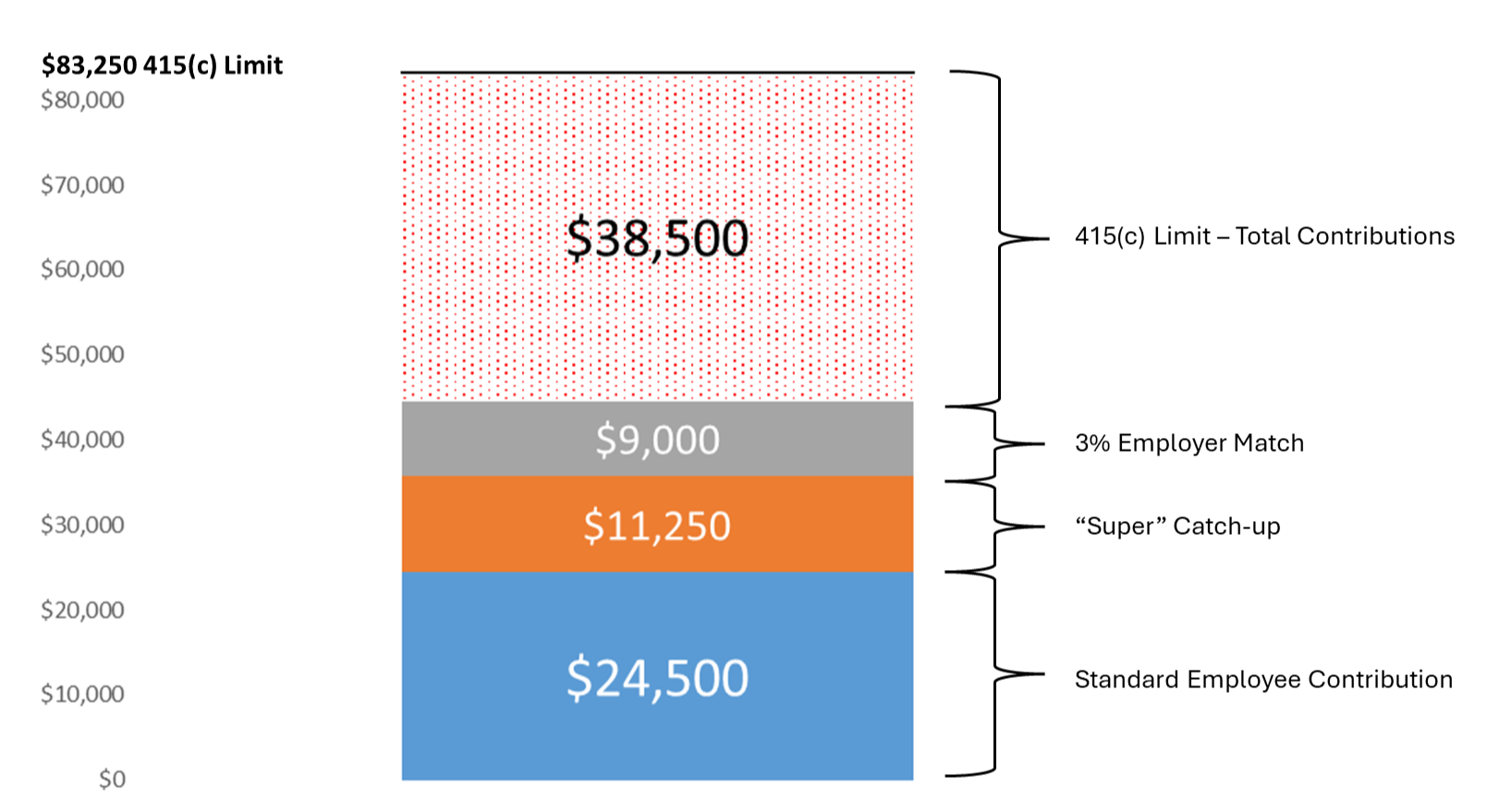

Example 2:

A 60-year-old earning $300,000, maxing out employee deferrals (including the “super” catch-up), with a 3% employer match and no employer profit-sharing.

In this instance, assuming the plan allowed it, this individual could make a $38,500 after-tax contribution to their 401(k).

Bottom Line

Given the modest annual Roth IRA contribution limit ($7,500, 2026) and income phaseout rules, the Mega Backdoor Roth presents an opportunity for high-income earners to build significant retirement savings in a tax-advantaged account and benefit from long-term, tax-free growth.

Since we can’t forecast future tax rates, building a tax-free “bucket” of Roth assets can be an effective way to prepare for retirement. Unlike pre-tax retirement account dollars, Roth accounts are not subject to required minimum distributions (RMDs), making them a valuable source of tax-free income later in retirement.

That said, the Mega Backdoor Roth strategy requires specific qualified retirement plan features and sufficient cashflow, so it won’t make sense for everyone. For those looking for additional savings opportunities but aren’t sure whether their plans allow it, please reach out. We’d be happy to review your plan with you.