As if you needed another reminder that year-end is quickly approaching, here are twelve quick but meaningful planning ideas to consider as we close out the calendar year. These ideas can help you maximize retirement, minimize taxes, and even make a difference to loved ones or charities. You’ll also find a handy download with key retirement, HSA, and estate planning limits.

1. Maximize Your Retirement

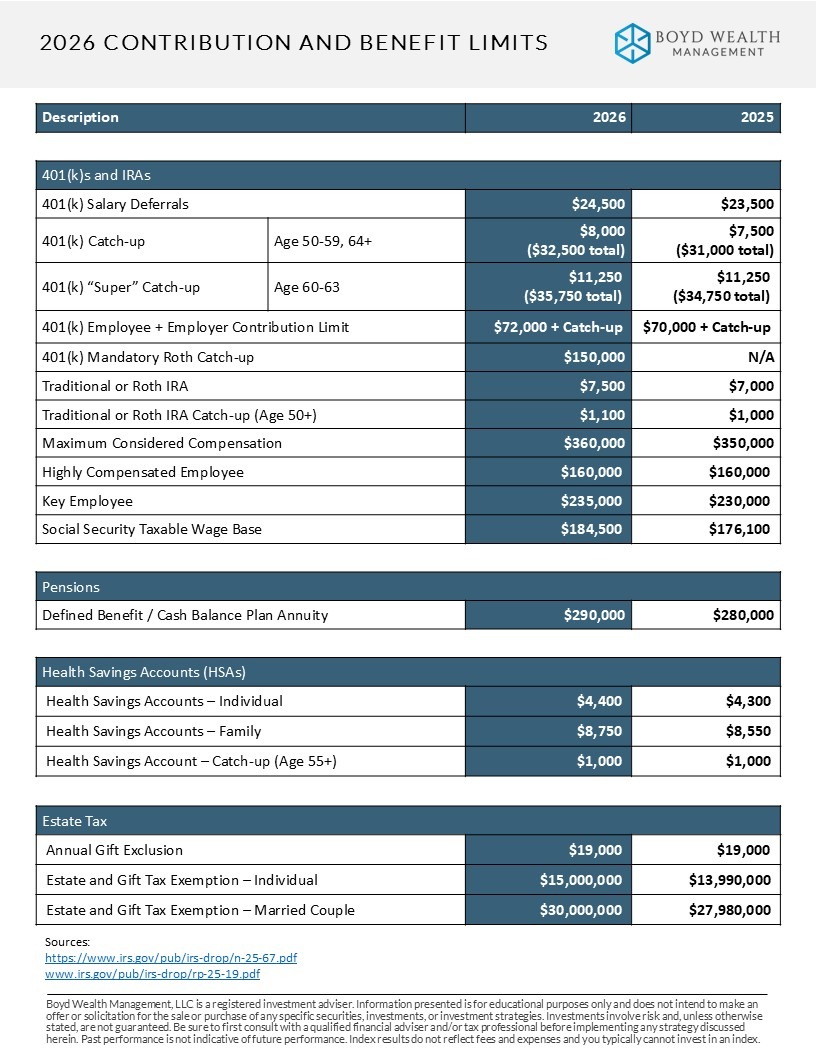

The IRS recently released their Contribution and Benefit Limits for 2026.

401(k) participants under the age of 50 will be getting a bump in how much they can contribute by $1,000 to $24,500.

Catch-up contribution:

- Individuals ages 50-59 and 64+ are allowed an $8,000 catch-up contribution (an increase of $500), for a total contribution of $32,500.

“Super” Catch-up contribution (initially introduced for 2025):

- Individuals ages 60-63 are allowed a $11,250 “super” catch-up contribution (unchanged), for a total contribution of $35,750.

Contribution limits for Traditional and Roth IRAs increased from $7,000 to $7,500. While Traditional and Roth IRA catch-up contributions for individuals aged 50 and older increased from $1,000 to $1,100.

You can download this chart for future reference here: 2026 Contribution and Benefit Limits

NEW FOR 2026

Mandatory Roth 401(k) Catch-up Contributions:

Starting in 2026, plan participants aged 50 and older whose FICA wages exceeded $150,000 in 2025 will be required to make their catch-up contributions as after-tax Roth contributions.

This policy was originally part of SECURE 2.0 and scheduled to take effect in 2024, but implementation was delayed due to significant administrative challenges for plan sponsors and recordkeepers.

It’s important to note that this provision applies only to individuals with W-2 wages over $150,000 in 2025. Business owners may have some flexibility in managing this threshold. For example:

- Self-employed individuals (sole proprietors and partners) are not affected because their compensation is not considered wages.

- S-Corp owners may have more control over their FICA wages and could consider keeping compensation below the threshold, provided the amount remains reasonable for their role and industry.

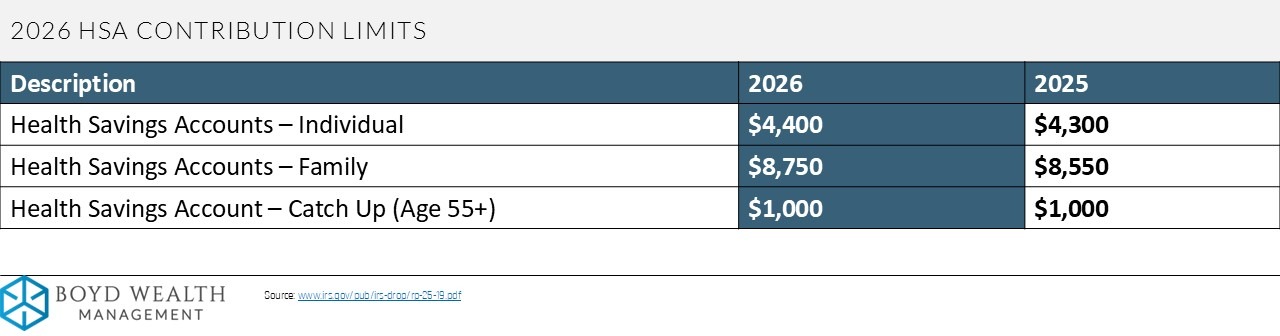

2. Maximize Your Health Savings Account (HSA)

HSAs can be a powerful savings tool for high income families. In fact, they are the only investment vehicle that delivers triple-tax benefits: contributions are tax-deductible, earnings grow tax-deferred, and withdrawals are tax-free when used for qualified medical expenses.

You can read more about how high-net-worth families use HSAs here.

If you are covered under a high-deductible-health-plan you have the option to make a tax-deductible contribution to your HSA.

For 2026, a high-deductible-health-plan (HDHP) is defined as one which requires minimum annual out-of-pocket deductibles of $1,700 for an individual and $3,400 for families. Yearly out-of-pocket expenses (including deductibles, copayments, and coinsurance) cannot be more than $8,500 for an individual or $17,000 for a family. You also must not be enrolled in Medicare, covered by another health plan that is not a high-deductible-health-plan, or claimed as a dependent on someone else’s tax return.

You have until April 15th, 2026 to maximize contributions and have them count toward the 2025 tax year.

Planning Tip:

Unlike retirement accounts, HSA contributions do not require earned income. Meaning, deductible HSA contributions are an excellent tool for early retirees to further reduce taxable income and potentially qualify for additional tax benefits or federal subsidies.

3. Review Your Healthcare Options During Open Enrollment

You may have missed it, but one of the main drivers behind the recent 40-day government shutdown was the state of our healthcare industry. As it currently stands, COVID-era Affordable Care Act (ACA) enhanced subsidies are set to expire on December 31st, 2025. Whether you agree with these subsidies or not, the reality is that healthcare costs are expected to rise significantly for most households in 2026.

Which is why this year’s open enrollment season is especially important. Take time to review your options and ensure you’re enrolled in a plan that meets both your healthcare needs and your budget. Consider factors like premiums, deductibles, maximum out-of-pocket limits, and prescription coverage to avoid surprises in the year ahead.

You can read more about Affordable Care Act subsidies here.

You can read more about Medicare enrollment here.

4. Maximize Your Charitable Contributions

The One Big Beautiful Bill Act (OBBBA) was signed into law on July 4th, 2025, and introduced several policies expected to reshape the tax code, affecting most taxpayers. Among its key provisions, the bill permanently extended federal ordinary income tax brackets, permanently increased the estate tax exemption and temporarily increased the deductibility of State and Local Taxes (SALT). However, it also added two policies that will significantly limit the deductibility of charitable donations starting in 2026.

So, if you plan to make substantial charitable gifts in the coming years, we highly suggest “bunching” your donations into a Donor-Advised Fund (DAF) before year-end. Doing so enables you to secure a full income tax deduction in 2025 and avoid the limitations that take effect in 2026. Your DAF contributions continue to grow tax-free and can be distributed to charities at any time, according to your timeline.

You can read more about DAFs and making the most of your charitable contributions in our Charitable Planning Guide.

You can read more about the OBBBA here.

You can read more about the OBBBA’s charitable deduction provisions here.

Planning Tip:

Cash is not always the most efficient asset to give to charity. Consider donating highly appreciated securities to a Donor-Advised Fund (or directly to a charity) to maximize your charitable contribution and minimize taxes.

5. Required Minimum Distributions (RMDs), IRA Contributions, and 529s

The SECURE Act was initially passed by Congress at the end of 2019 and intended to improve retirement savings opportunities, hence the acronym “Setting Every Community Up for Retirement Enhancement”. It was a big deal at the time, the most significant piece of retirement legislation since the 2006 Pension Protection Act.

Congress came together to pass SECURE 2.0 at the end of 2022, building on this popular legislation and clarifying some of its provisions.

The SECURE 2.0 Act includes 92 new provisions designed to promote savings, add incentives for businesses to offer retirement plans to their employees, and provide more overall flexibility to those saving for retirement. Here are some notable points:

- The update pushed back the starting date for Required Minimum Distributions (RMDs) from IRAs/401(k)s to age 73 (if you reach age 72 after December 31st, 2022). The original law was age 70½, the SECURE Act made it age 72, and now, the RMD age will increase again in 2033 to age 75! This allows savers more time for additional compound growth and tax deferral in their retirement plans.

- Contributions to Traditional IRAs can be made at any age. Under original rules, contributions were disallowed after reaching 70½. If you have earned income and a desire to pad your Traditional IRA, there’s still time to make a contribution prior to April 15th.

- Starting in 2024, 529 College Savings plan account holders can move money to a Roth IRA under certain conditions. You can read more here.

Planning Tip:

If you turned 73 years old in 2025, you have until April 1st of 2026 to take your first RMD. However, that means you’ll take two RMDs in the same calendar year. Subsequent RMDs must be taken by December 31st annually thereafter.

For 529 Plans, remember to reimburse yourself for all those qualified college expenses. All reimbursements must be made in the year the expense was incurred.

6. Make a Qualified Charitable Distribution (QCD)

One of the most exciting aspects of the Pension Protection Act of 2006 was the Qualified Charitable Distribution, or QCD. A QCD allows you to make a charitable donation directly out of an Individual Retirement Account, or IRA, up to a maximum of $108,000 per person in 2025 and will increase to $111,000 per person in 2026. The amount donated directly offsets the Required Minimum Distribution, or RMD.

High-net-worth individuals in the RMD stage are typically receiving more in required distributions than they want or need. By donating to your favorite charity directly from an IRA or an Inherited IRA, your required distribution and taxes are reduced under the QCD method. This is especially important for those unable to itemize their deductions, as one can still receive the full benefit of their charitable donation while claiming the standard deduction. If you’re currently taking RMDs or expect significant future RMDs, and are making charitable donations, QCD’s can be a fantastic strategy.

You can learn more about QCDs here.

Planning Tip:

Review your current and planned charitable contributions. If you're 70½ or older, consider donating directly from your IRA in preparation for your future RMDs. You can make QCDs as soon as you reach age 70½, even though RMDs don’t begin until age 73.

401(k) and 403(b) are ineligible for QCDs, but you can simply rollover your employer plan to an IRA if you wish to execute such a transaction.

7. Gifting to Loved Ones

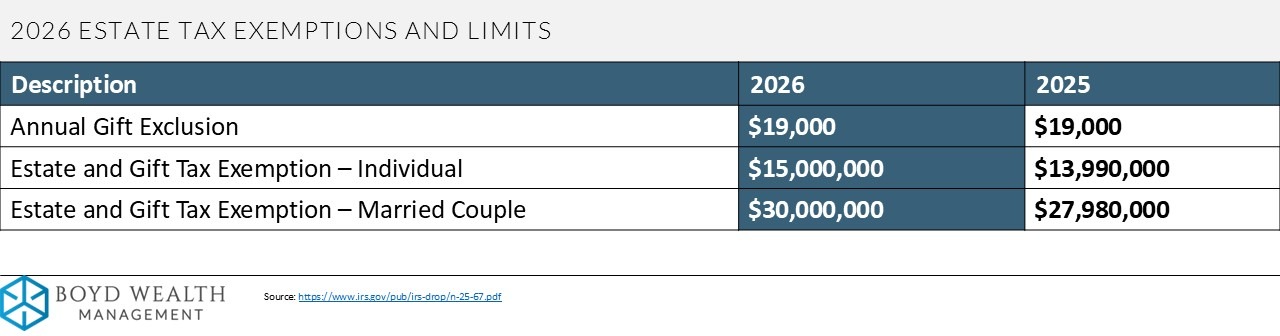

The estate tax exemption is $13,990,000 per person in 2025 and increases to $15,000,000 in 2026.

For those above these exemption amounts, a federal estate tax is levied at a 40% rate on all assets above the exemption (the rate is 18-39% up to $1,000,000 and then 40% on anything above that, so we use 40% for simplicity).

You can make tax-free gifts up to $19,000 per person this year. Annual gifts do not rollover, so make your gifts before year-end.

For 2026, the annual gift exclusion will remain at $19,000 per person.

Planning Tip:

Since the annual gifting limit is $19,000 per person in 2025, a husband and wife with two married children and four grandchildren could gift a total of $304,000 in 2025 without affecting their lifetime gift and estate tax exemption. That’s $19,000 for each of the 8 family members, from both husband and wife, or $38,000 x 8!

8. Tax-Loss Harvesting

The market has delivered attractive returns for the past few years, but not all sectors, asset classes, or individual securities have participated. Some of the portfolio holdings in your taxable investment account may have losses that you can harvest for tax purposes.

Tax-loss harvesting is the process of selling an investment that has dropped in value below an investor’s cost basis to lock in a paper loss. The investor then reinvests the sale proceeds into a different security that still meets their overall investment risk profile and asset allocation strategy. The recognized loss can then be used to offset taxable gains in other parts of the portfolio, or it can be carried over to offset capital gains in future years.

For our clients, you’ve likely noticed us harvesting losses throughout the year whenever opportunities arose.

Planning Tip:

2025 may be a great time to divest from concentrated stock positions that have historically carried large, embedded capital gains. You can reinvest into a diversified portfolio and use capital losses harvested from this year (or those carried forward on your return from 2024) to offset some or all of those realized gains.

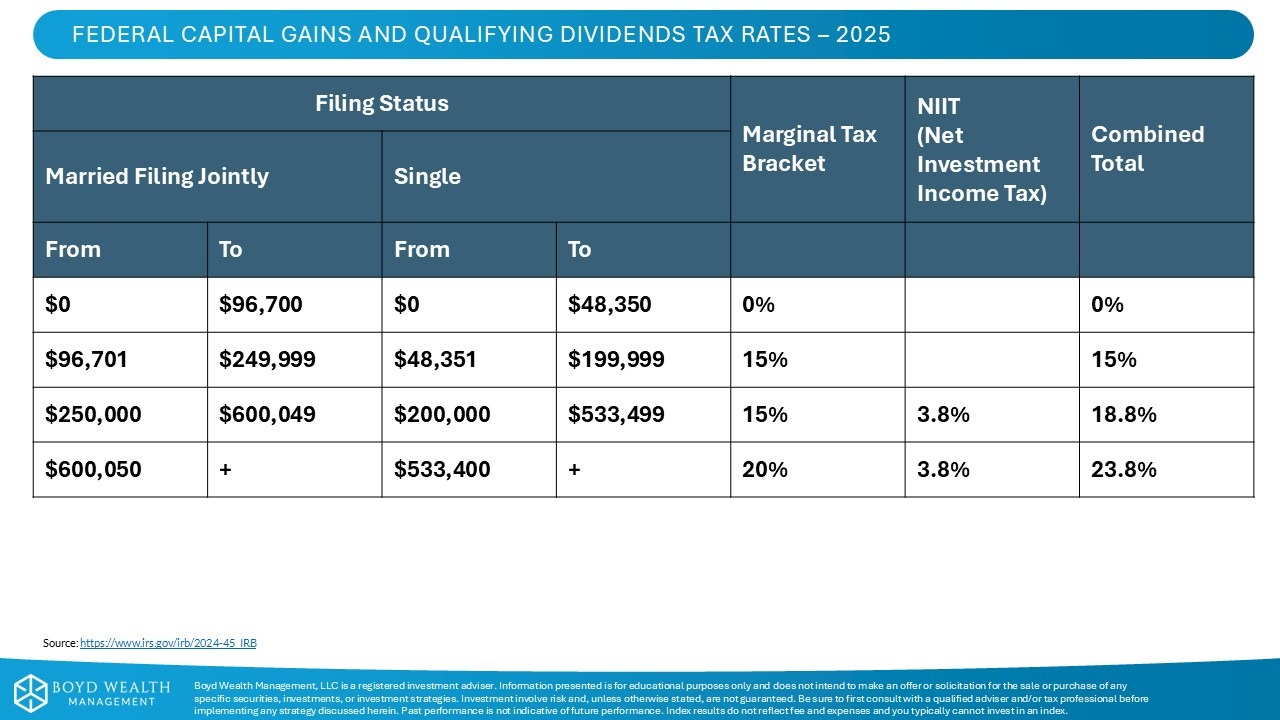

9. Tax-Gain Harvesting

Conversely, if you are experiencing a low taxable income year, you might consider harvesting gains in your non-qualified / taxable accounts.

Tax-gain harvesting works the opposite of loss harvesting, where an investor deliberately realizes capital gains to take advantage of favorable tax rates and increase their cost basis. See below

- Single filers can realize capital gains at a 0% tax rate if their taxable income is $48,350 or less.

- Joint filers can realize capital gains at a 0% tax rate if their taxable income is $96,700 or less.

You can read more about tax-gain harvesting here.

Planning Tip:

The strong performance in 2025 may present an opportunity to realize capital gains from concentrated positions with minimal tax consequences, while reallocating the proceeds into a more diversified portfolio.

10. Roth Conversions

If there is not an immediate reliance on your investment assets for retirement income, and you are experiencing a low taxable income year, consider converting all or a portion of a Traditional IRA to a Roth IRA. Doing so means you’ll recognize income today on the amount converted, but withdrawals in the future will be tax-free.

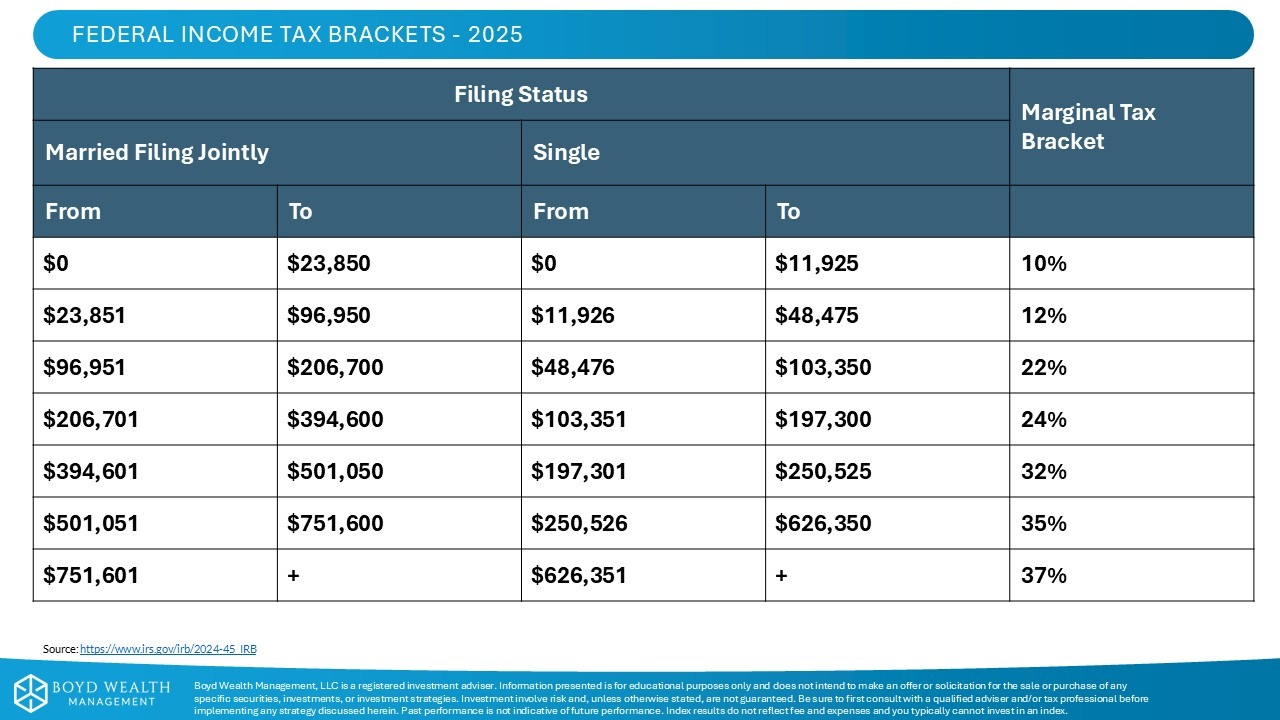

The first $11,925 of ordinary income (beyond standard or itemized deductions) for single filers and $23,850 for married filers carries just a 10% federal tax rate. The rate is only 12% up to $48,475 and $96,950 respectively. You may consider converting up to the max of the first two brackets if your expected income in the future (earned income, Required Minimum Distributions, Pension, etc.) will be higher.

If you’re carrying an ordinary loss on your tax return, you could convert Traditional IRAs to Roth essentially tax-free as the loss will offset the income from the conversion.

Planning Tip:

Converting from Traditional to Roth is not an all or nothing proposition. You can make partial conversions and spread them out over several years.

11. Tax-Efficient Withdrawal Sequencing

Conversely, if there is an immediate need for income from your investment assets, and you are in a low taxable income year, consider splitting withdrawals between retirement and non-retirement accounts. Doing so means you may recognize more taxable income today but could significantly reduce the overall amount of taxes paid over the remainder of your lifetime.

Planning Tip:

The idea is to utilize taxable distributions from your Traditional / pre-tax retirement accounts to fill the lower 10% and 12% federal bracket(s). If left to compound uninterrupted, retirement account balances can grow rather quickly, often resulting in larger annual RMDs than may be needed in the future. This can lead to higher ordinary income tax rates, a higher percentage of social security benefits being taxed, and a potential increase in Medicare premiums due to monthly surcharges later in retirement.

You can learn more about how Social Security benefits are taxed here.

12. Update Your Beneficiary Designations

The end of the year is a great time to make sure your beneficiaries are current. Log into your 401(k) plan, speak with your HR administrator, pull up your IRAs and life insurance policies, and request a review of your beneficiary designations to verify that they match your current wishes.

Life transitions, such as divorce or the death of a spouse, are incredibly difficult. It’s understandable that during these challenging times, beneficiary designations are sometimes overlooked and left unchanged. This is your reminder to review them.

Planning Tip:

Whatever you have listed on a beneficiary form usually overrides what is written in your will or trust. A beneficiary form provides its own direction for the asset it covers, so make sure it accurately reflects your wishes.

Now is an ideal time to review these twelve year-end planning tips, as even one of them can make a positive difference in your plan.

Please reach out to us to talk through any of these planning opportunities in more detail.

Happy Holidays,

Colby Dotson